How To Calculate Monthly Payment On A Loan

adminse

Apr 06, 2025 · 7 min read

Table of Contents

Decoding the Numbers: A Comprehensive Guide to Calculating Loan Monthly Payments

What if understanding loan repayment was as simple as a few keystrokes? Mastering loan payment calculations empowers you to make informed financial decisions, securing your future with confidence.

Editor’s Note: This article on calculating monthly loan payments was published today, providing you with the most up-to-date information and formulas to accurately determine your repayment schedule. This guide covers various methods, from simple manual calculations to using online tools and understanding the intricacies of amortization schedules.

Why Calculating Monthly Loan Payments Matters:

Understanding how to calculate your monthly loan payments is crucial for several reasons. It allows you to budget effectively, compare loan offers, and avoid unforeseen financial strain. Whether you're buying a car, a house, or consolidating debt, knowing your monthly obligations empowers you to make responsible financial choices. This knowledge is relevant across various industries, from personal finance to real estate, and impacts both businesses and individuals. Accurate calculations ensure you can plan for future expenses and avoid defaulting on your loan. Furthermore, understanding the amortization schedule, explained later, can help you strategize for early loan repayment and save on interest.

Overview: What This Article Covers:

This article provides a comprehensive guide to calculating monthly loan payments. We will explore different methods, including manual calculation using the standard formula, employing online calculators, and understanding amortization schedules. We will also examine factors influencing monthly payments, such as interest rates, loan terms, and down payments.

The Research and Effort Behind the Insights:

This article draws upon established financial principles and formulas, widely used in personal finance and banking. Information presented is based on universally accepted calculations and methodologies. We have also reviewed various online loan calculators to verify the accuracy of the methods discussed. The goal is to provide readers with a clear, accurate, and accessible understanding of loan payment calculations.

Key Takeaways:

- Understanding the Loan Payment Formula: Learn the core formula and its components.

- Manual Calculation Techniques: Master the step-by-step process of calculating monthly payments.

- Utilizing Online Loan Calculators: Explore the advantages and ease of use of online tools.

- Amortization Schedules: Understand how loan payments are allocated over time.

- Factors Influencing Monthly Payments: Analyze the impact of interest rates, loan terms, and down payments.

Smooth Transition to the Core Discussion:

Now that we understand the importance of calculating loan payments, let's delve into the specifics of how it's done. We'll begin with the fundamental formula and progress to more advanced concepts.

Exploring the Key Aspects of Calculating Loan Monthly Payments:

1. The Loan Payment Formula:

The most common formula used to calculate the monthly payment on a loan is:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount (the total amount borrowed)

- i = Monthly Interest Rate (Annual Interest Rate / 12)

- n = Total Number of Payments (Loan Term in Years * 12)

This formula, while seemingly complex, is straightforward when broken down step-by-step.

2. Manual Calculation Techniques:

Let’s illustrate with an example:

Suppose you borrow $10,000 (P) at an annual interest rate of 5% (Annual Interest Rate) for 3 years (Loan Term).

-

Calculate the monthly interest rate (i): 5% annual interest / 12 months = 0.05 / 12 = 0.004167

-

Calculate the total number of payments (n): 3 years * 12 months/year = 36 months

-

Apply the formula:

M = 10000 [ 0.004167 (1 + 0.004167)^36 ] / [ (1 + 0.004167)^36 – 1]

- Solve the equation: This requires calculating exponents and performing the arithmetic. A scientific calculator is highly recommended for this step. The calculation will yield a monthly payment (M) of approximately $299.70.

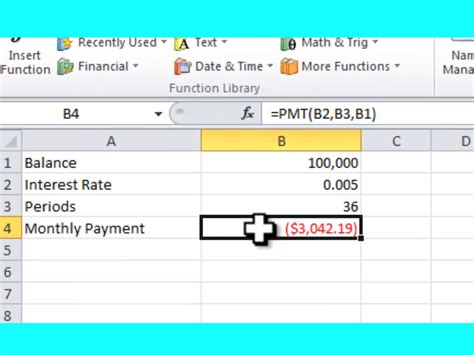

3. Utilizing Online Loan Calculators:

Thankfully, you don't need to manually perform these complex calculations every time. Numerous free online loan calculators are readily available. Simply input the loan amount, interest rate, and loan term, and the calculator instantly provides the monthly payment. These calculators often offer additional features, such as amortization schedules and the total interest paid over the loan's life.

4. Amortization Schedules:

An amortization schedule details the breakdown of each monthly payment into principal and interest. In the initial months of a loan, a larger portion of the payment goes towards interest, while the principal repayment increases gradually over time. Understanding your amortization schedule allows you to see exactly how your loan is being repaid and can be valuable for financial planning and early repayment strategies. Many online loan calculators will generate an amortization schedule for you.

5. Factors Influencing Monthly Payments:

Several factors significantly impact your monthly loan payment:

- Interest Rate: Higher interest rates result in higher monthly payments. Shopping around for loans with competitive interest rates is crucial.

- Loan Term: Longer loan terms generally result in lower monthly payments but lead to paying significantly more interest over the life of the loan. Shorter loan terms mean higher monthly payments but lower overall interest costs.

- Loan Amount: A larger loan amount naturally translates to higher monthly payments. A down payment reduces the principal loan amount, thus lowering monthly payments.

Exploring the Connection Between Interest Rates and Loan Monthly Payments:

The interest rate is arguably the most influential factor in determining your monthly loan payment. A seemingly small difference in interest rates can significantly affect your overall repayment cost. For example, a 1% increase in the annual interest rate on a $200,000 mortgage could result in thousands of dollars more in interest paid over the life of the loan. This underscores the importance of securing the lowest possible interest rate when borrowing.

Key Factors to Consider:

-

Roles and Real-World Examples: Consider a car loan scenario. A 3% interest rate on a $20,000 loan over 5 years will have a much lower monthly payment compared to a 10% interest rate over the same period.

-

Risks and Mitigations: Failing to secure a favorable interest rate due to poor credit or insufficient research can lead to significantly higher monthly payments and overall loan costs. Mitigating this risk involves improving credit scores, comparing loan offers meticulously, and potentially negotiating interest rates with lenders.

-

Impact and Implications: The cumulative impact of higher monthly payments due to a high interest rate can restrict financial flexibility, limit savings, and potentially lead to financial hardship.

Conclusion: Reinforcing the Connection:

The relationship between interest rates and monthly loan payments is paramount. A thorough understanding of this dynamic is crucial for making responsible borrowing decisions. By carefully considering interest rates alongside other factors, borrowers can optimize their loan terms and achieve financial stability.

Further Analysis: Examining Interest Rate Fluctuations in Greater Detail:

Interest rates are not static; they fluctuate based on various economic factors. Understanding these fluctuations allows for better financial planning. Market conditions, inflation, and central bank policies all influence interest rates. Keeping an eye on these indicators can inform borrowing decisions and provide opportunities to secure favorable interest rates.

FAQ Section: Answering Common Questions About Calculating Loan Monthly Payments:

Q: What is the most accurate way to calculate my monthly loan payment?

A: The most accurate method is using the standard loan payment formula or a reputable online loan calculator. Manual calculations require careful attention to detail, while online calculators offer speed and convenience.

Q: Can I use a simple interest calculation instead of the compound interest formula?

A: No, the standard loan payment formula uses compound interest, which accurately reflects how interest accumulates over time. Simple interest calculations would be significantly inaccurate and underestimate your monthly payment.

Q: What if my loan has additional fees or charges?

A: Most online loan calculators allow you to factor in additional fees, such as origination fees or closing costs. This will provide a more accurate reflection of your total monthly obligation.

Q: How can I reduce my monthly loan payment?

A: You can try to negotiate a lower interest rate, increase your down payment (if applicable), or extend the loan term (keeping in mind the increased overall interest cost).

Practical Tips: Maximizing the Benefits of Understanding Loan Payment Calculations:

-

Understand the Basics: Familiarize yourself with the loan payment formula and its components.

-

Utilize Online Calculators: Use online loan calculators to quickly and accurately determine your monthly payments.

-

Compare Loan Offers: Compare offers from multiple lenders to find the most favorable interest rate and terms.

-

Create a Realistic Budget: Incorporate your calculated monthly loan payment into your budget to ensure affordability.

-

Review Your Amortization Schedule: Track your loan repayment progress and plan for potential early payoff strategies.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding how to calculate monthly loan payments is a fundamental skill for navigating personal finance. By mastering this process and considering the various factors involved, you can make informed decisions, secure favorable loan terms, and achieve long-term financial stability. The tools and knowledge provided in this article empower you to take control of your financial future. Remember, responsible borrowing begins with a thorough understanding of the numbers.

Latest Posts

Latest Posts

-

What Does A 790 Credit Score Mean

Apr 06, 2025

-

What Can I Get With A 790 Credit Score

Apr 06, 2025

-

How Common Is A 790 Credit Score

Apr 06, 2025

-

How To Qualify For Navy Federal Credit Union

Apr 06, 2025

-

How To Increase Navy Federal Credit Card Limit

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about How To Calculate Monthly Payment On A Loan . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.