What Is A Grace Period How Long Is A Typical Grace Period

adminse

Apr 02, 2025 · 9 min read

Table of Contents

Understanding Grace Periods: How Long is the Typical Grace Period and What Does it Mean?

What if missing a payment didn't immediately result in penalties? Grace periods offer a crucial buffer, allowing individuals and businesses to rectify overlooked payments without immediate repercussions.

Editor’s Note: This article on grace periods was published today, providing readers with up-to-date information on this crucial financial concept. We explore the various types of grace periods, their typical durations, and the importance of understanding their implications.

Why Grace Periods Matter: Relevance, Practical Applications, and Industry Significance

Grace periods are a vital component of many financial agreements, offering a safety net for unforeseen circumstances. Whether it's a missed credit card payment, a late loan installment, or a delayed insurance premium, a grace period provides a temporary reprieve before penalties are applied. This buffer reduces the risk of immediate negative consequences, allowing individuals and businesses time to rectify the situation and avoid damaging their credit scores or incurring substantial fees. Understanding grace periods is crucial for responsible financial management and avoiding unnecessary financial hardship. The applications span various sectors, impacting personal finance, business operations, and insurance policies.

Overview: What This Article Covers

This article provides a comprehensive overview of grace periods, encompassing their definition, types, typical durations across various financial products, implications of missing the grace period, and strategies for avoiding late payments. Readers will gain a solid understanding of how grace periods function and how to leverage them effectively to manage their finances responsibly.

The Research and Effort Behind the Insights

This article draws upon extensive research, including analysis of financial regulations, industry best practices, and case studies from various financial institutions. Information presented here is sourced from reputable financial websites, consumer protection agencies, and legal documents. The goal is to provide accurate and reliable information to empower readers with informed decision-making.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of what a grace period is and its core principles.

- Types of Grace Periods: Exploring different grace periods across various financial products.

- Typical Durations: Examining the common lengths of grace periods for loans, credit cards, and insurance.

- Consequences of Missing the Grace Period: Understanding the penalties associated with late payments after the grace period expires.

- Strategies for Avoiding Late Payments: Practical tips for managing finances effectively and preventing missed payments.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding grace periods, let's delve deeper into their intricacies, exploring the various types, typical durations, and associated implications.

Exploring the Key Aspects of Grace Periods:

1. Definition and Core Concepts:

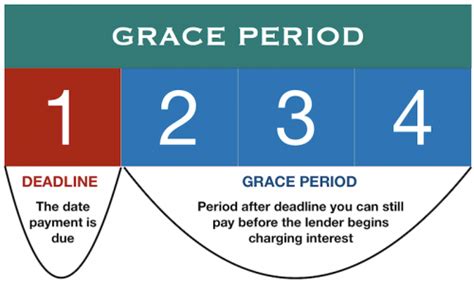

A grace period is a short period of time following a due date during which a payment can be made without incurring late fees or penalties. It essentially offers a temporary reprieve, acknowledging that unforeseen circumstances can sometimes cause delays in payments. The specific terms and conditions of the grace period, including its duration and any associated stipulations, are typically outlined in the agreement governing the financial product.

2. Types of Grace Periods:

Grace periods are not a one-size-fits-all concept. Their application and duration vary significantly depending on the financial product involved:

-

Credit Card Grace Periods: Most credit cards offer a grace period on purchases. This means that if you pay your balance in full by the due date, you won't be charged any interest on the purchases made during the previous billing cycle. However, cash advances usually do not qualify for this grace period and accrue interest immediately. The length of the credit card grace period typically ranges from 21 to 25 days.

-

Loan Grace Periods: Loans, such as student loans, personal loans, and mortgages, may also include grace periods. These grace periods are often offered during periods of transition, such as after graduation for student loans or during periods of unemployment (under specific conditions). The length of loan grace periods varies significantly depending on the type of loan and the lender's policies. They can range from a few months to several years.

-

Insurance Grace Periods: Many insurance policies, such as health insurance or auto insurance, provide a grace period during which the policy remains active even if the premium payment is late. The length of this grace period can vary, but it's often between 30 and 60 days. However, coverage may be suspended during the grace period in some cases.

-

Utility Grace Periods: Utility companies, such as electricity, gas, and water providers, sometimes offer grace periods before disconnecting service for non-payment. The duration of these grace periods is typically shorter than those offered by financial institutions and may depend on the company's policies and local regulations.

3. Typical Durations:

The typical duration of a grace period significantly depends on the specific financial product. As highlighted above, credit card grace periods are usually around 21-25 days, while loan grace periods can range from months to years depending on the loan type and lender's policies. Insurance grace periods often fall between 30 and 60 days. Utility grace periods tend to be the shortest, typically lasting a week or two.

4. Consequences of Missing the Grace Period:

Failing to make a payment within the grace period carries significant consequences. These consequences can include:

-

Late Fees: The most common consequence is the imposition of a late payment fee. These fees can vary significantly depending on the creditor or insurer.

-

Higher Interest Rates: For credit cards and some loans, missing the grace period can lead to an increase in the interest rate, making it more expensive to repay the debt.

-

Negative Impact on Credit Score: Late payments are reported to credit bureaus, which negatively impacts your credit score. This can make it harder to obtain future loans or credit at favorable terms.

-

Account Suspension or Termination: In some cases, especially with utilities and insurance, failure to pay within the grace period may result in service suspension or policy cancellation.

5. Strategies for Avoiding Late Payments:

To avoid the negative consequences of missing grace periods, it's essential to adopt proactive financial management strategies:

-

Set Reminders: Use calendar reminders, budgeting apps, or online banking features to set reminders for upcoming payments.

-

Automate Payments: Consider setting up automatic payments to ensure timely payments each month.

-

Budget Effectively: Create a realistic budget that accounts for all your expenses and ensures sufficient funds are allocated for payments.

-

Monitor Accounts Regularly: Regularly check your accounts to ensure payments are processed correctly and that you're aware of upcoming due dates.

-

Communicate with Creditors: If you anticipate difficulty making a payment, contact your creditor or insurer as soon as possible to discuss possible payment arrangements or extensions.

Closing Insights: Summarizing the Core Discussion

Grace periods provide a valuable safety net in the world of personal finance. Understanding their application, typical durations, and associated implications is crucial for responsible financial management. By adopting proactive strategies and communicating with creditors, individuals and businesses can mitigate the risks of late payments and maintain a healthy financial standing.

Exploring the Connection Between Credit Scores and Grace Periods

The relationship between credit scores and grace periods is significant. While a grace period itself doesn't directly impact your credit score, missing a payment during the grace period almost always leads to a negative impact on your credit score. This highlights the importance of understanding and utilizing grace periods responsibly.

Key Factors to Consider:

Roles and Real-World Examples: A poor credit score resulting from late payments (even within a grace period) can lead to higher interest rates on future loans, difficulty securing new credit, and even rejection for rental applications or employment opportunities. For instance, someone consistently missing credit card payments may see their credit score plummet, resulting in a significant increase in interest rates on subsequent loans or even the inability to secure a mortgage.

Risks and Mitigations: The primary risk is the damage to your credit score and the associated financial consequences. Mitigations include proactively managing finances, setting up payment reminders, and communicating with creditors if there are financial difficulties.

Impact and Implications: The long-term impact of consistently missing payments, even during grace periods, can be severe, significantly impacting access to credit and financial opportunities for years to come.

Conclusion: Reinforcing the Connection

The interplay between credit scores and grace periods is critical. While grace periods offer a temporary buffer, failing to utilize them responsibly can have significant long-term repercussions. Prioritizing timely payments and actively managing finances is crucial for maintaining a healthy credit score and overall financial well-being.

Further Analysis: Examining Credit Reporting Agencies in Greater Detail

Credit reporting agencies (CRAs) play a vital role in this connection. They collect and aggregate payment history information from various lenders and insurers. Late payments, even those occurring after the grace period, are reported to CRAs, negatively impacting your credit score. Understanding how CRAs operate and what factors contribute to your credit score is essential for responsible credit management.

FAQ Section: Answering Common Questions About Grace Periods

Q: What happens if I don't pay within the grace period?

A: Failing to make a payment within the grace period will typically result in late fees, potentially higher interest rates, a negative impact on your credit score, and in some cases, account suspension or termination.

Q: How long is a grace period for a student loan?

A: The length of a grace period for a student loan varies significantly depending on the type of loan and lender policies. It could range from a few months to several years, often starting after graduation.

Q: Can I negotiate an extension of my grace period?

A: You can attempt to negotiate an extension with your lender or insurer, but it's not always guaranteed. It's essential to contact them as soon as you anticipate difficulties in making a timely payment.

Q: Are grace periods always the same length?

A: No, grace period durations vary substantially depending on the type of financial product (credit card, loan, insurance, utility) and the lender or provider's policies.

Practical Tips: Maximizing the Benefits of Grace Periods

-

Understand the Terms: Carefully review the terms and conditions of your agreements to understand the specific grace period details for each financial product.

-

Use Reminders: Employ calendar reminders or budgeting apps to track payment due dates and avoid missing them.

-

Automate Payments: Set up automatic payments to ensure timely payments, eliminating the risk of human error.

-

Budget Wisely: Create a detailed budget to allocate sufficient funds for all your financial obligations.

-

Communicate Proactively: Contact your creditors or insurers immediately if you anticipate payment difficulties to explore possible solutions.

Final Conclusion: Wrapping Up with Lasting Insights

Grace periods offer a valuable financial buffer, but their effectiveness hinges on responsible financial management. By understanding the implications of grace periods, utilizing proactive strategies, and communicating openly with creditors, individuals can navigate the financial landscape more confidently and avoid the negative consequences of late payments. Mastering the use of grace periods is a crucial step toward building strong financial habits and maintaining a healthy credit score.

Latest Posts

Latest Posts

-

How To Apply For Navy Federal Credit Union

Apr 06, 2025

-

Which Credit Cards Give The Highest Credit Limits

Apr 06, 2025

-

What Card Has The Highest Credit Limit

Apr 06, 2025

-

What Is The Highest Credit Limit For Capital One Gold Mastercard

Apr 06, 2025

-

What Is The Highest Credit Limit You Can Get On A Credit Card

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Is A Grace Period How Long Is A Typical Grace Period . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.