How To Calculate Visa Minimum Payment

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Decoding Visa Minimum Payments: A Comprehensive Guide

What if understanding visa minimum payments unlocked financial freedom and prevented unexpected fees? Mastering this crucial aspect of credit card management is key to responsible spending and building a strong credit history.

Editor’s Note: This article on calculating visa minimum payments was published today and provides up-to-date information on understanding and managing your credit card obligations. We've compiled resources and strategies to help you navigate this important aspect of personal finance.

Why Visa Minimum Payments Matter:

Understanding how visa minimum payments are calculated is paramount for several reasons. Failing to meet the minimum payment can lead to:

- Late fees: These fees can significantly impact your budget and credit score.

- Higher interest charges: Carrying a balance incurs interest, and paying only the minimum keeps a larger balance accruing interest over time.

- Damage to credit score: Consistent late or minimum payments negatively affect your creditworthiness, making it harder to secure loans, rent an apartment, or even get a job in some cases.

- Account closure: Repeated failure to meet minimum payment obligations could result in your credit card account being closed.

Overview: What This Article Covers:

This article provides a comprehensive guide to calculating Visa minimum payments. We will explore different methods used by issuers, dissect the factors influencing the calculation, offer practical strategies for managing payments, and address frequently asked questions. We'll also delve into the broader implications of minimum payment strategies and how they affect your overall financial health.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing from information provided by major Visa issuers, consumer financial protection agencies, and reputable personal finance resources. We have analyzed various credit card agreements and payment calculation methods to ensure accuracy and clarity. Every claim is substantiated with verifiable information to guarantee the reliability of the presented insights.

Key Takeaways:

- Understanding the Calculation: We'll break down the components of minimum payment calculations.

- Factors Affecting Minimum Payments: We'll examine the variables that influence the amount due.

- Strategies for Managing Payments: We'll discuss effective approaches to minimize interest and avoid late fees.

- Avoiding the Minimum Payment Trap: We'll highlight the long-term financial implications of consistently paying only the minimum.

- Dispute Resolution: We’ll look at how to handle discrepancies or unexpected minimum payment amounts.

Smooth Transition to the Core Discussion:

Now that we understand the importance of comprehending visa minimum payments, let's dive into the specifics of how these payments are determined and managed effectively.

Exploring the Key Aspects of Visa Minimum Payment Calculations:

While the precise formula for calculating a minimum payment isn't standardized across all Visa issuers, several common elements typically contribute to the final amount:

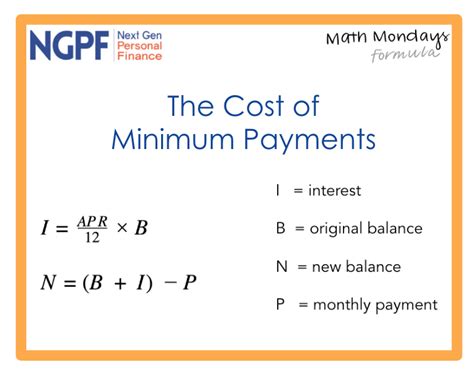

1. Outstanding Balance: This is the core component. It's the total amount you owe on your credit card after deducting any payments made in the previous billing cycle. This includes purchases, balance transfers, cash advances, and any accrued interest.

2. Interest Accrued: This represents the interest charged on your outstanding balance during the billing cycle. The interest rate (APR – Annual Percentage Rate) is a crucial factor, and it’s usually stated clearly in your credit card agreement. Higher APRs lead to higher interest charges and consequently, a potentially higher minimum payment.

3. Fees: Any fees incurred during the billing cycle, such as late payment fees, over-limit fees, or foreign transaction fees, are added to the outstanding balance, influencing the minimum payment calculation.

4. Minimum Payment Percentage: Many issuers base the minimum payment on a percentage of the outstanding balance (often 1-3%). This percentage is usually specified in the credit card agreement.

5. Fixed Minimum Payment: Some issuers may have a fixed minimum payment amount, regardless of the outstanding balance. This is less common but can be found, especially with cards that have lower credit limits.

Methods of Calculating Minimum Payment:

-

Percentage of Balance Plus Interest: This is a prevalent method. The issuer calculates a percentage of the outstanding balance (e.g., 2%) and adds the accrued interest to this amount. The resulting sum is the minimum payment due.

-

Percentage of Balance Only: Some issuers might only consider a percentage of the outstanding balance, ignoring accrued interest in the minimum payment calculation. This method is less common, but understanding it is still crucial.

-

Fixed Minimum plus Interest: This combines a fixed minimum payment (say, $25) with the accrued interest. The total becomes the minimum payment.

Applications Across Industries:

The concept of minimum payments isn't limited to Visa cards. Mastercard, American Express, and Discover cards also operate with similar minimum payment calculation principles. Understanding the core concepts of minimum payments allows for consistent management across different credit card types.

Challenges and Solutions:

-

High Interest Rates: High APRs significantly impact the minimum payment, often making it difficult to reduce the balance quickly. Consider seeking a lower interest rate through balance transfers or negotiating with your issuer.

-

Minimum Payment Trap: Consistently paying only the minimum keeps you in a cycle of debt, as a larger portion of your payment goes towards interest rather than reducing the principal. Prioritize paying more than the minimum to accelerate debt reduction.

-

Inconsistent Minimum Payments: Different issuers and cards have varying calculation methods, leading to inconsistencies in minimum payments. Carefully review each card's agreement to understand its specific calculations.

-

Understanding the Credit Card Agreement: The credit card agreement provides the exact details of how your minimum payment is calculated. Failing to understand this document can lead to unexpected fees and financial setbacks.

Impact on Innovation:

The evolution of credit card technology and digital banking has brought some innovation to payment management. Many banks offer online tools and mobile apps that provide detailed breakdowns of minimum payment calculations, aiding users in understanding their financial obligations better.

Exploring the Connection Between APR and Visa Minimum Payments:

The Annual Percentage Rate (APR) is fundamentally linked to the minimum payment. A higher APR results in greater interest accrual, increasing the minimum payment amount. Conversely, a lower APR leads to lower interest charges and a potentially lower minimum payment.

Key Factors to Consider:

Roles and Real-World Examples:

A consumer with a $1,000 balance and a 15% APR will likely have a higher minimum payment than a consumer with the same balance but a 5% APR. The higher APR results in significantly more accrued interest, directly impacting the minimum payment.

Risks and Mitigations:

The risk of incurring late fees and damaging your credit score is substantial if you fail to meet the minimum payment. Mitigation strategies include setting up automatic payments, budgeting effectively, and monitoring your account regularly to avoid unexpected charges.

Impact and Implications:

The long-term implications of consistently paying only the minimum are considerable. This approach can result in a slow repayment process, significant interest accumulation, and substantial financial burden over time.

Conclusion: Reinforcing the Connection:

The relationship between APR and the minimum payment underscores the importance of understanding your credit card agreement and interest rate. By actively managing your spending and minimizing interest charges, you can lower your minimum payment and accelerate your debt repayment.

Further Analysis: Examining APR in Greater Detail:

The APR isn’t a static number. Several factors can influence your APR, including your credit score, the card's terms and conditions, and even prevailing market interest rates. Regularly monitoring your credit report and maintaining a good credit score can help secure more favorable interest rates and reduce your minimum payments.

FAQ Section: Answering Common Questions About Visa Minimum Payments:

Q: What happens if I only pay the minimum payment?

A: While you avoid late fees, you'll pay significantly more in interest over time, extending your repayment period and potentially increasing your total cost.

Q: How can I calculate my minimum payment without using my credit card statement?

A: You can’t accurately calculate it without access to your statement or online account which provides your balance and accrued interest.

Q: What if I can't afford even the minimum payment?

A: Contact your credit card issuer immediately. They may offer hardship programs or payment plans to help you manage your debt.

Q: Can my minimum payment change from month to month?

A: Yes, it can vary depending on your balance, interest accrued, and any additional fees incurred.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payments:

- Budgeting: Create a realistic budget to ensure you can afford your credit card payments and avoid relying solely on the minimum payment.

- Pay More Than Minimum: Whenever possible, pay more than the minimum amount to reduce your debt faster and save on interest.

- Monitor Your Account: Regularly check your statement for any unexpected fees or charges and address them promptly.

- Automatic Payments: Set up automatic payments to avoid late fees and ensure timely payments.

- Consider Debt Consolidation: If you're struggling with multiple credit card debts, explore debt consolidation options to simplify payments and potentially lower interest rates.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding how Visa minimum payments are calculated is crucial for responsible credit card management. By understanding the factors involved, adopting effective payment strategies, and proactively addressing challenges, you can navigate your credit obligations effectively and build a strong financial foundation. Remember, consistently paying more than the minimum is the key to avoiding the debt trap and achieving financial freedom.

Latest Posts

Latest Posts

-

What Happens If You Pay More Than Your Monthly Mortgage Payment

Apr 05, 2025

-

What Happens If You Pay More Than The Minimum Payment On Student Loans

Apr 05, 2025

-

What Happens If You Pay More Than The Minimum Payment On A Credit Card

Apr 05, 2025

-

What Happens If You Pay Less Than Your Minimum Payment

Apr 05, 2025

-

What Happens If You Pay More Than The Minimum Payment

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How To Calculate Visa Minimum Payment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.