What Happens If You Pay More Than The Minimum Payment

adminse

Apr 05, 2025 · 8 min read

Table of Contents

What happens if you pay more than the minimum payment?

Making extra payments can significantly accelerate debt repayment and save you substantial money over time.

Editor’s Note: This article on the implications of paying more than the minimum payment on your debts has been meticulously researched and updated to reflect current financial practices. It provides practical strategies for managing debt effectively and achieving financial freedom.

Why Paying More Than the Minimum Matters: Relevance, Practical Applications, and Financial Significance

Many people struggle with debt, often feeling trapped by minimum payments. The belief that “paying the minimum is enough” is a costly misconception. Paying more than the minimum payment on your credit cards, loans, and other debts has significant implications for your overall financial health. It impacts your credit score, reduces the total interest paid, and ultimately accelerates your path to becoming debt-free. This article will explore these implications in detail, arming you with the knowledge to make informed decisions about your debt repayment strategy.

Overview: What This Article Covers

This comprehensive guide delves into the intricacies of exceeding minimum payments, examining its effect on interest accrual, credit scores, and long-term financial well-being. We’ll analyze various debt repayment methods, offer practical strategies for maximizing extra payments, and address common concerns and misconceptions surrounding this financial practice. Readers will gain actionable insights, empowering them to take control of their finances and achieve significant savings.

The Research and Effort Behind the Insights

This article is the product of extensive research, drawing upon reputable sources such as the Consumer Financial Protection Bureau (CFPB), financial literacy organizations, and peer-reviewed studies on consumer debt management. We've analyzed data on interest rates, credit scoring models, and debt repayment strategies to ensure accuracy and provide readers with reliable, actionable information.

Key Takeaways:

- Reduced Interest Payments: The most significant benefit of paying more than the minimum is the substantial reduction in total interest paid over the life of the loan or credit card debt.

- Faster Debt Repayment: Extra payments directly reduce the principal balance, leading to quicker debt elimination and financial freedom.

- Improved Credit Score: Lowering your credit utilization ratio (the percentage of available credit used) by paying down balances can positively impact your credit score.

- Increased Financial Flexibility: Becoming debt-free sooner frees up funds for other financial goals like saving, investing, or homeownership.

- Reduced Financial Stress: Knowing you're actively chipping away at your debt can significantly reduce financial anxiety and improve overall well-being.

Smooth Transition to the Core Discussion:

With a firm understanding of the significant advantages of paying above the minimum, let's delve into the specifics, exploring the mechanics of interest accrual, strategic repayment methods, and practical steps you can take to optimize your debt repayment journey.

Exploring the Key Aspects of Paying More Than the Minimum Payment

1. Understanding Interest Accrual:

Credit cards and loans accrue interest daily on the outstanding balance. The minimum payment often barely covers the interest charged, meaning your principal balance remains largely unchanged. By paying more than the minimum, you directly reduce the principal, leading to less interest accruing in subsequent billing cycles. This snowball effect accelerates debt reduction.

2. The Power of the Snowball and Avalanche Methods:

Two popular debt repayment strategies are the debt snowball and debt avalanche methods. Both involve paying more than the minimum on your debts, but they differ in their approach:

-

Debt Snowball Method: This method prioritizes paying off the smallest debt first, regardless of interest rate. The psychological boost of quickly eliminating a debt can motivate continued repayment efforts. Once the smallest debt is cleared, you roll that payment amount into the next smallest debt, creating a snowball effect.

-

Debt Avalanche Method: This method focuses on paying off the debt with the highest interest rate first. While it might not provide the same initial psychological boost, it ultimately saves more money on interest in the long run.

3. Calculating the Impact of Extra Payments:

To understand the true impact of paying extra, utilize online debt repayment calculators. These tools allow you to input your debt details, including interest rates and minimum payments, and simulate the effect of adding extra payments. This will show you how much faster you can become debt-free and how much you'll save in interest.

4. Strategic Allocation of Extra Funds:

When deciding how to allocate extra funds, prioritize debts with the highest interest rates first (avalanche method) or the smallest balance first (snowball method). You may also choose to focus on high-interest debts that carry a higher risk of penalties or negative impact on your credit score.

5. The Impact on Your Credit Score:

While paying more than the minimum significantly impacts your debt repayment speed and interest costs, its impact on your credit score is less straightforward. A lower credit utilization ratio (the percentage of your available credit that you're using) is generally beneficial to your credit score. Paying down balances significantly reduces this ratio, typically leading to a boost in your score. However, aggressively paying off multiple debts within a short period can, at times, cause a small temporary dip before the benefit of a lower utilization ratio takes hold.

Closing Insights: Summarizing the Core Discussion

Paying more than the minimum payment is not just a good idea; it's a crucial step towards achieving financial freedom and security. By understanding the mechanics of interest accrual, employing effective repayment strategies, and monitoring your progress, you can significantly accelerate your debt repayment journey and save thousands of dollars in interest over the life of your debts.

Exploring the Connection Between Emergency Funds and Extra Debt Payments

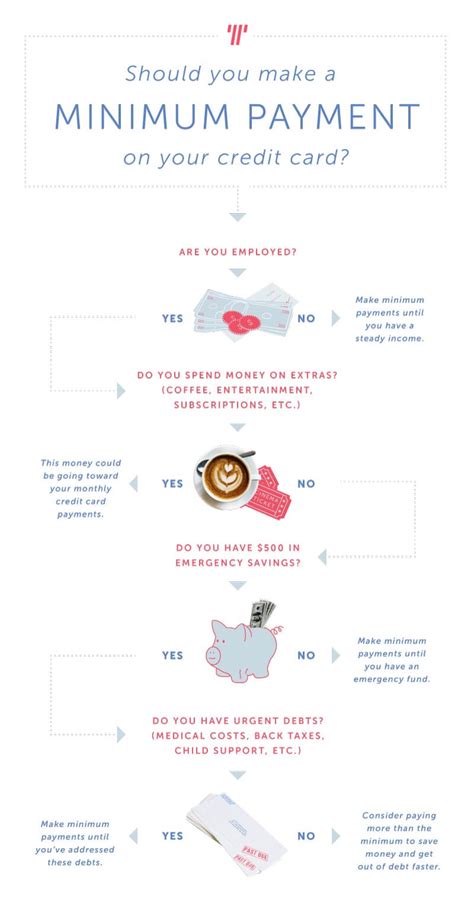

A crucial aspect often overlooked is the relationship between maintaining an emergency fund and making extra debt payments. While diligently paying down debt is essential, neglecting to build an emergency fund is risky. Unexpected expenses can derail even the best-laid debt repayment plans, potentially forcing you to use high-interest credit cards to cover unforeseen costs, setting you back financially.

Key Factors to Consider:

-

Roles and Real-World Examples: Imagine losing your job or facing a major car repair. Without an emergency fund, you might be forced to rely on high-interest credit cards, accumulating more debt and undoing progress made on your repayment plan.

-

Risks and Mitigations: The risk of depleting savings to pay down debts is that you leave yourself vulnerable to unforeseen events. The mitigation involves building a 3-6 month emergency fund before aggressively paying down debt. This fund acts as a safety net, allowing you to handle unexpected expenses without derailing your debt repayment plan.

-

Impact and Implications: The interplay between emergency funds and debt repayment is a balancing act. Prioritize building an emergency fund first, creating a stable foundation before focusing intensely on debt elimination.

Conclusion: Reinforcing the Connection

The relationship between emergency funds and extra debt payments is vital for sustainable financial health. While aggressive debt repayment is commendable, it should be approached strategically. Building a financial safety net protects your progress, ensuring you won't be forced back into debt due to unforeseen circumstances.

Further Analysis: Examining Emergency Funds in Greater Detail

An emergency fund provides a financial cushion to handle unexpected expenses without incurring debt. Ideally, this fund should cover 3-6 months of essential living expenses. Regular contributions, even small amounts, are key to building this vital safety net. Once established, you can allocate more resources to accelerate debt repayment, knowing you have a financial safety net in place.

FAQ Section: Answering Common Questions About Paying More Than the Minimum Payment

-

Q: What if I can only afford a slightly higher payment than the minimum? A: Even small extra payments make a difference over time. Every extra dollar reduces the principal and ultimately saves on interest.

-

Q: Will paying extra affect my credit score negatively? A: Generally, no. Paying down balances improves your credit utilization ratio, which is usually a positive factor in credit scoring. However, temporarily closing accounts or dramatically decreasing utilization too rapidly might slightly affect your score before the overall benefits become apparent.

-

Q: Should I pay off debt or invest? A: This depends on several factors, including your debt interest rates, your risk tolerance, and your investment goals. High-interest debt should be prioritized.

-

Q: What if I have multiple debts with different interest rates? A: Prioritize debts with the highest interest rates (avalanche method) or the smallest balance (snowball method), based on your personal preferences and motivation.

Practical Tips: Maximizing the Benefits of Paying More Than the Minimum Payment

-

Automate Your Payments: Set up automatic payments to ensure consistent extra payments each month.

-

Track Your Progress: Monitor your debt balances and interest payments regularly to stay motivated and track your savings.

-

Budget Effectively: Create a realistic budget to identify areas where you can cut expenses and allocate more funds toward debt repayment.

-

Seek Professional Advice: If overwhelmed by debt, consult a financial advisor or credit counselor for personalized guidance.

-

Explore Debt Consolidation: Consider debt consolidation options to simplify your payments and potentially lower your interest rate.

Final Conclusion: Wrapping Up with Lasting Insights

Paying more than the minimum payment on your debts is a powerful tool for achieving financial freedom. By understanding the mechanics of interest accrual, utilizing effective repayment strategies, and building a strong financial foundation, you can significantly improve your financial health and secure your future. Remember, consistent effort and strategic planning are key to successfully navigating the path to debt freedom. Take control of your finances today, and reap the rewards of a debt-free tomorrow.

Latest Posts

Latest Posts

-

How Much Does The Bible Talk About Money

Apr 06, 2025

-

What Does The Bible Said About Money

Apr 06, 2025

-

What Does The Bible Say About Wealth Management

Apr 06, 2025

-

What Does The Bible Say About Money Management Pdf

Apr 06, 2025

-

Money Management Dalam Trading

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Happens If You Pay More Than The Minimum Payment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.