How To Calculate Minimum Monthly Payment On A Loan

adminse

Apr 06, 2025 · 7 min read

Table of Contents

Unlocking the Mystery: How to Calculate Minimum Monthly Loan Payments

What if understanding your minimum monthly loan payment could save you thousands of dollars over the life of a loan? Mastering this calculation empowers you to make informed financial decisions and avoid costly pitfalls.

Editor’s Note: This article provides a comprehensive guide to calculating minimum monthly loan payments, equipping you with the knowledge to navigate personal finance effectively. We explore various methods, address common scenarios, and offer practical tips for managing your debt responsibly.

Why Understanding Minimum Monthly Payments Matters

Understanding your minimum monthly payment is crucial for several reasons. It directly impacts your budgeting, debt management strategy, and overall financial health. Failing to understand this fundamental calculation can lead to late payments, increased interest charges, and potentially even default. Knowing your minimum payment allows you to:

- Create a Realistic Budget: Accurately incorporating loan payments into your monthly budget ensures you can afford your other expenses.

- Avoid Late Fees and Penalties: Making at least the minimum payment on time prevents costly penalties and damages your credit score.

- Strategically Manage Debt: Understanding your minimum payment helps you decide if you need to explore debt consolidation, balance transfers, or other strategies to lower your overall debt burden.

- Monitor Loan Progress: Tracking your payments against the minimum allows you to see how quickly you are paying down your principal.

Overview: What This Article Covers

This article provides a detailed explanation of how to calculate minimum monthly loan payments using several methods, including the standard formula and readily available online calculators. We'll delve into the impact of interest rates, loan terms, and loan types on your minimum payment. Furthermore, we'll explore potential scenarios and offer practical tips for managing your loan repayments effectively.

The Research and Effort Behind the Insights

The information presented in this article is based on established financial principles and widely accepted formulas for loan amortization. We’ve consulted numerous reputable financial websites, textbooks, and regulatory guidelines to ensure accuracy and clarity. The calculations and examples provided are designed to be easily understood and replicated by anyone, regardless of their financial background.

Key Takeaways:

- Understanding Loan Amortization: The process of paying off a loan over time, including interest payments.

- The Standard Formula: The mathematical equation used to calculate minimum monthly payments.

- Using Online Calculators: The convenience and simplicity of using online tools.

- Impact of Interest Rates and Loan Terms: How these factors significantly influence monthly payments.

- Managing Your Loan Repayments: Practical strategies for budgeting and staying on track.

Smooth Transition to the Core Discussion

With a clear understanding of why calculating minimum monthly payments is essential, let’s delve into the mechanics and explore the different methods available for determining this critical figure.

Exploring the Key Aspects of Calculating Minimum Monthly Loan Payments

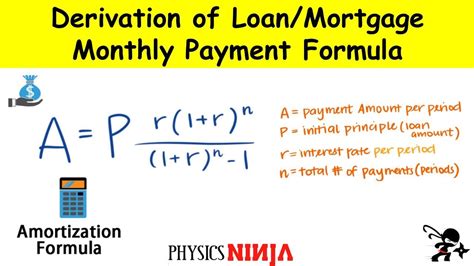

1. The Standard Formula:

The most accurate way to calculate your minimum monthly payment involves using a formula that accounts for the principal loan amount, the interest rate, and the loan term. The formula is based on the concept of loan amortization, which is the process of gradually paying off a loan's principal and interest over a set period.

The formula is as follows:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount (the initial amount borrowed)

- i = Monthly Interest Rate (annual interest rate divided by 12)

- n = Total Number of Payments (loan term in years multiplied by 12)

Example:

Let's say you borrow $10,000 at an annual interest rate of 5% for a loan term of 3 years.

- P = $10,000

- i = 0.05 / 12 = 0.004167 (approximately)

- n = 3 years * 12 months/year = 36

Plugging these values into the formula:

M = 10000 [ 0.004167 (1 + 0.004167)^36 ] / [ (1 + 0.004167)^36 – 1]

M ≈ $299.70

Therefore, the minimum monthly payment for this loan would be approximately $299.70.

2. Using Online Calculators:

While the formula provides precise results, using an online loan calculator offers a simpler and more user-friendly approach. Numerous websites offer free loan calculators; you simply input the loan amount, interest rate, and loan term, and the calculator will instantly generate the minimum monthly payment. This method eliminates the need for manual calculations and reduces the risk of errors. Many calculators also provide a detailed amortization schedule, showing the breakdown of principal and interest payments over the life of the loan.

3. Impact of Interest Rates and Loan Terms:

The interest rate and loan term significantly affect the minimum monthly payment. A higher interest rate leads to a higher minimum payment because you're paying more in interest charges. Similarly, a longer loan term results in a lower monthly payment, but you'll pay significantly more in total interest over the life of the loan. Conversely, a shorter loan term results in a higher monthly payment but substantially less total interest paid. Understanding this trade-off is crucial for making informed borrowing decisions.

Exploring the Connection Between APR and Minimum Monthly Payments

The Annual Percentage Rate (APR) is a crucial factor influencing your minimum monthly payment. The APR represents the total cost of borrowing, including interest and any associated fees. A higher APR means a higher minimum monthly payment, as you're paying more interest charges over the loan's duration. It’s vital to compare APRs across different lenders to secure the most favorable terms.

Key Factors to Consider:

- Roles and Real-World Examples: Consider two loans with the same principal but different APRs. A loan with a 7% APR will have a higher minimum payment than one with a 5% APR.

- Risks and Mitigations: A high APR increases the risk of debt accumulation if you can't afford the higher monthly payment. Mitigation strategies could include exploring lower-interest loans or shortening the loan term.

- Impact and Implications: The long-term impact of a high APR is significant; you will pay much more interest overall, increasing the total cost of the loan.

Conclusion: Reinforcing the Connection

The relationship between the APR and your minimum monthly payment is directly proportional. A higher APR results in a higher minimum payment, emphasizing the importance of securing the lowest possible APR when borrowing money. Careful consideration of the APR is essential for responsible debt management and informed financial decisions.

Further Analysis: Examining APR in Greater Detail

The APR calculation incorporates various factors besides the basic interest rate, including origination fees, processing fees, and other charges. Understanding these components helps you accurately compare loan offers. Always inquire about all associated fees before committing to a loan to ensure you are comparing apples to apples.

FAQ Section: Answering Common Questions About Minimum Monthly Loan Payments

- What happens if I only pay the minimum payment? While you'll avoid late fees, you'll pay more interest over time, extending the loan's duration and increasing the total cost.

- Can I pay more than the minimum payment? Absolutely! Paying more than the minimum reduces the principal faster, lowering the total interest paid and shortening the loan's term.

- What if I miss a minimum payment? Missing payments will lead to late fees, negatively impacting your credit score, and potentially incurring further penalties from the lender.

- How do I find my minimum payment amount? Check your loan agreement or use an online loan calculator with your loan details.

Practical Tips: Maximizing the Benefits of Understanding Minimum Monthly Loan Payments

- Budgeting: Integrate your minimum payment into your monthly budget to ensure you can consistently meet your obligations.

- Debt Tracking: Use spreadsheets or budgeting apps to track your loan progress and ensure you are making at least the minimum payment on time.

- Debt Reduction Strategies: Explore options like debt consolidation or balance transfers to lower interest rates and simplify debt management.

- Financial Planning: Factor loan repayments into your long-term financial plan to ensure you can manage debt responsibly and achieve your financial goals.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding how to calculate your minimum monthly loan payment is a fundamental skill for responsible financial management. By using the standard formula or online calculators, you can accurately determine your minimum payment, create a realistic budget, and avoid the pitfalls of late payments and accumulating debt. Mastering this calculation empowers you to make informed decisions and navigate your financial journey with greater confidence and control. Remember, while the minimum payment keeps you compliant, proactively paying more than the minimum is a powerful strategy for accelerating debt reduction and saving significant money in the long run.

Latest Posts

Latest Posts

-

What Percentage Should You Keep Your Credit Utilization

Apr 06, 2025

-

What Percentage Should You Keep Your Credit Utilization Below

Apr 06, 2025

-

What Percentage Should You Keep Your Credit Utilization Under

Apr 06, 2025

-

What Percentage Should I Keep My Credit Utilization

Apr 06, 2025

-

How Good Is 790 Credit Rating

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about How To Calculate Minimum Monthly Payment On A Loan . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.