What Is The Minimum Payment On A $600 Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Payment on a $600 Credit Card: A Comprehensive Guide

What if navigating your credit card payments felt less like a minefield and more like a clear path to financial freedom? Understanding the minimum payment on your $600 credit card is the crucial first step.

Editor’s Note: This article on minimum credit card payments, specifically concerning a $600 balance, was published today to provide up-to-date information and actionable advice for managing credit card debt. We strive to offer clear, accurate guidance to empower responsible financial decisions.

Why Understanding Minimum Payments Matters:

A $600 credit card balance might seem manageable, but failing to understand the implications of minimum payments can lead to a snowball effect of debt, significantly impacting your credit score and financial well-being. Understanding your minimum payment isn't just about avoiding late fees; it's about strategically managing your debt and building a strong financial future. This knowledge empowers you to make informed choices about repayment strategies and avoid the hidden pitfalls of minimum payment plans. This article will cover everything from calculating your minimum payment to exploring the long-term consequences of only making the minimum payment. The information presented here is relevant to anyone managing credit card debt, regardless of the balance amount.

Overview: What This Article Covers:

This in-depth guide will dissect the intricacies of minimum credit card payments, focusing on a $600 balance. We will explore how minimum payments are calculated, the hidden costs associated with this payment method, the impact on your credit score, and ultimately, how to create a more effective repayment strategy. We will also delve into the crucial connection between interest rates and minimum payments, exploring how variations in interest rates significantly affect the overall cost of your debt. Finally, we’ll address frequently asked questions and offer practical tips for minimizing debt and building a healthier financial outlook.

The Research and Effort Behind the Insights:

This article is based on extensive research into credit card regulations, financial best practices, and analysis of various credit card agreements. Information from reputable sources such as the Consumer Financial Protection Bureau (CFPB), leading financial institutions, and consumer finance experts has been incorporated to ensure accuracy and clarity. The insights presented are data-driven and intended to provide actionable guidance for readers.

Key Takeaways:

- Understanding Minimum Payment Calculation: Learn how credit card issuers determine your minimum payment.

- Hidden Costs of Minimum Payments: Discover the long-term financial implications of only making minimum payments.

- Impact on Credit Score: Explore how minimum payment strategies affect your creditworthiness.

- Interest Rate's Influence: Understand the critical role of interest rates in determining your overall repayment costs.

- Developing Effective Repayment Strategies: Learn how to create a plan to pay off your debt more efficiently.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding minimum payments, let's delve into the specifics of calculating your minimum payment on a $600 credit card balance and explore the associated costs and implications.

Exploring the Key Aspects of Minimum Payments:

1. Definition and Core Concepts:

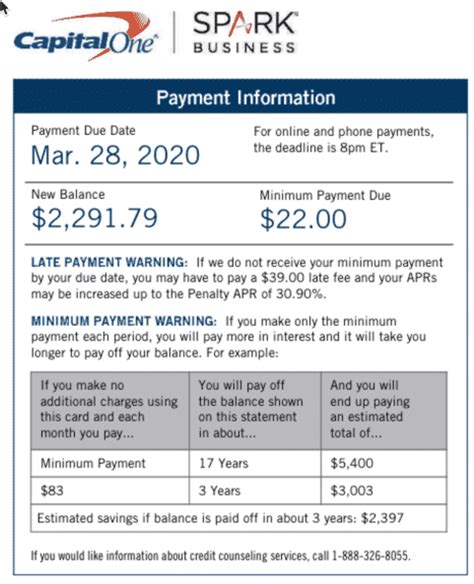

The minimum payment is the smallest amount a credit card company requires you to pay each month to avoid late payment fees and maintain your account in good standing. This amount is typically a percentage of your outstanding balance (often between 1% and 3%), but it can also include a fixed minimum dollar amount, or a combination of both. This means a minimum payment on a $600 balance might range from $6 to $18, depending on your credit card's terms.

2. Applications Across Industries:

The concept of minimum payments is consistent across most major credit card issuers. However, the specific calculation method and the minimum payment percentage can vary depending on your credit card agreement. Some cards may offer a higher minimum payment percentage during the introductory period and then lower it after a certain time.

3. Challenges and Solutions:

The primary challenge with minimum payments is that they often lead to prolonged repayment periods and significantly higher overall interest costs. The solution is to pay more than the minimum whenever possible, accelerating debt reduction and minimizing interest charges.

4. Impact on Innovation:

The credit card industry has seen some innovations aimed at helping consumers manage debt more effectively, such as balance transfer cards and debt consolidation loans. However, these methods should be approached cautiously and only after careful consideration of associated fees and terms.

Closing Insights: Summarizing the Core Discussion:

Simply making the minimum payment on a credit card is often a costly and time-consuming strategy. While it keeps your account active and prevents late fees, it significantly prolongs the repayment process, ultimately leading to considerably higher interest expenses. Understanding this dynamic is crucial for effective debt management.

Exploring the Connection Between Interest Rates and Minimum Payments:

The interest rate is the percentage charged on your outstanding credit card balance. Higher interest rates dramatically impact the effectiveness of minimum payments. If you only make the minimum payment, a significant portion of your payment goes towards covering the interest, leaving only a small amount to reduce your principal balance. This means you'll be paying interest on interest, escalating the total cost of your debt over time. For example, a $600 balance with a 20% APR (annual percentage rate) will incur substantial interest charges if only minimum payments are made.

Key Factors to Consider:

Roles and Real-World Examples:

Imagine two scenarios: One where you make only the minimum payment of $15 per month on a $600 balance with a 20% APR, and another where you pay $100 per month. The first scenario will take significantly longer to repay the debt and result in much higher interest charges. The second scenario, while demanding a larger monthly payment, leads to quicker debt elimination and lower overall interest payments.

Risks and Mitigations:

The primary risk of relying on minimum payments is the spiraling debt and the accruing interest. To mitigate this risk, prioritize paying more than the minimum whenever possible. Develop a budget, explore strategies to increase income, or cut unnecessary expenses to allocate more funds towards debt repayment.

Impact and Implications:

The long-term impact of consistently making only the minimum payment includes a longer repayment period, significantly higher interest charges, potential damage to your credit score, and increased financial stress.

Conclusion: Reinforcing the Connection:

The relationship between interest rates and minimum payments is crucial for understanding the true cost of credit card debt. Higher interest rates, combined with minimum payment strategies, lead to a vicious cycle of debt, hindering financial progress.

Further Analysis: Examining Interest Rate Calculations in Greater Detail:

The calculation of interest on a credit card is typically done daily on your average daily balance. This means the interest charges are calculated on the outstanding balance throughout the billing cycle, not just on the balance at the beginning or end. Understanding this compounding interest is vital to grasp the long-term implications of only paying the minimum.

FAQ Section: Answering Common Questions About Minimum Payments:

Q: What happens if I miss a minimum payment?

A: Missing a minimum payment will result in late fees, negatively impacting your credit score and potentially increasing your interest rate.

Q: Can I negotiate a lower minimum payment with my credit card company?

A: While not always guaranteed, you can try contacting your credit card company to discuss options for managing your debt, but they might offer hardship programs or alternative solutions instead of a lower minimum payment.

Q: Is it always better to pay more than the minimum payment?

A: Yes, paying more than the minimum payment accelerates debt repayment, minimizes interest charges, and improves your financial health.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Use:

- Understand your credit card agreement: Know your interest rate, minimum payment calculation, and late payment fees.

- Create a realistic budget: Track your income and expenses to determine how much you can allocate to credit card repayment.

- Prioritize debt reduction: Focus on paying down your credit card debt as quickly as possible.

- Explore debt consolidation options: Consider consolidating high-interest debt into a lower-interest loan if feasible.

- Monitor your credit report: Regularly check your credit report for accuracy and identify any potential issues.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding the minimum payment on a $600 credit card, or any credit card for that matter, is essential for responsible debt management. While making the minimum payment prevents immediate penalties, it's a costly long-term strategy. By actively managing your debt, paying more than the minimum, and understanding the interplay of interest rates and minimum payments, you can break free from the cycle of debt and build a secure financial future. Take control of your finances; knowledge is power in the world of credit card management.

Latest Posts

Latest Posts

-

Cara Kerja Fund Manager

Apr 06, 2025

-

Cara Money Management

Apr 06, 2025

-

Money Management Group Activities

Apr 06, 2025

-

How To Become A Money Manager

Apr 06, 2025

-

Activities For Money Management

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A $600 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.