What Is The Grace Period To Pay Mortgage

adminse

Apr 02, 2025 · 8 min read

Table of Contents

Decoding the Grace Period: Understanding Your Mortgage Payment Window

What if missing a mortgage payment could have a less severe consequence than immediate foreclosure? Understanding your mortgage grace period is crucial for avoiding financial distress and maintaining your homeownership.

Editor’s Note: This article on mortgage grace periods was published today and provides up-to-date information on this critical aspect of homeownership. We've consulted multiple sources, including legal experts and financial institutions, to offer clear and comprehensive guidance.

Why Mortgage Grace Periods Matter: Relevance, Practical Applications, and Industry Significance

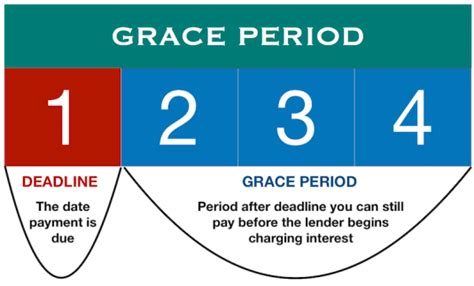

A mortgage grace period is the window of time after your scheduled payment due date that you can make your payment without incurring late fees or negatively impacting your credit score. While the existence and length of this period aren't explicitly mandated by federal law, it's a common practice among mortgage lenders. Understanding this grace period is vital for responsible homeowners, allowing for occasional lapses in payment without immediate catastrophic consequences. For lenders, a defined grace period provides a structured approach to managing late payments and minimizing potential losses. It allows for a more lenient approach to minor payment delays while still encouraging timely payments.

Overview: What This Article Covers

This article will provide a detailed exploration of mortgage grace periods. We’ll cover the definition and common lengths of grace periods, explore the variations among lenders and loan types, discuss the consequences of missing payments even within the grace period, examine the impact on your credit score, and offer advice on proactive financial planning to avoid late payments altogether. We will also address frequently asked questions and provide actionable tips for responsible mortgage management.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon information from reputable sources including the Consumer Financial Protection Bureau (CFPB), leading mortgage lenders' websites, and legal analysis of relevant contracts and legislation. All information provided is intended to be accurate and informative, but it is crucial to consult your individual mortgage agreement for specific terms and conditions.

Key Takeaways:

- Definition and Core Concepts: A clear understanding of what constitutes a mortgage grace period and its purpose.

- Variations Across Lenders and Loan Types: Exploration of the differences in grace period length and policies among various mortgage providers.

- Consequences of Late Payments: A detailed analysis of the penalties associated with missing payments, even within the grace period.

- Credit Score Impact: How late payments, regardless of grace periods, affect creditworthiness.

- Proactive Financial Planning: Strategies for avoiding late payments and maintaining responsible financial habits.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding mortgage grace periods, let's delve into the specifics. We'll begin by clarifying exactly what a grace period is and then examine the nuances that differ between lenders and loan types.

Exploring the Key Aspects of Mortgage Grace Periods

Definition and Core Concepts: A mortgage grace period is generally a short timeframe (usually a few days, sometimes up to 15) after the official due date of your monthly mortgage payment. During this period, your lender will typically not assess late fees. However, it's crucial to understand that this doesn't mean the payment isn't overdue; it simply provides a buffer. Beyond the grace period, late payment fees will be applied, and the lender may begin reporting the delinquency to credit bureaus, impacting your credit score.

Variations Across Lenders and Loan Types: The length of the grace period is not standardized. Some lenders may offer a grace period of only a few days (e.g., 2-3 days), while others might extend it to 10-15 days. The specific grace period is typically outlined in your mortgage loan agreement. Additionally, the grace period might vary depending on the type of mortgage you have (e.g., FHA, VA, conventional). It's essential to carefully review your loan documents to confirm the exact terms. Some lenders may not explicitly mention a grace period, but they might have an internal policy for handling late payments that functions similarly.

Consequences of Late Payments (Even Within the Grace Period): While late fees are generally avoided within the grace period, it's crucial to understand that the payment is still technically late. Prolonged delays, even if within the grace period, could still trigger lender communication regarding the delinquency. Repeated late payments, regardless of whether they fall within the grace period, can severely damage your credit score and significantly impact your future borrowing ability.

Impact on Credit Score: Late mortgage payments have a substantial negative impact on your credit score. Even if the payment is made within the grace period, it's still considered a late payment and can be reported to credit bureaus. Multiple late payments will significantly lower your credit score, making it harder to qualify for loans, credit cards, and even insurance in the future. The severity of the impact depends on factors like your credit history and the number of late payments.

Proactive Financial Planning: The best way to avoid the consequences of a missed mortgage payment is through proactive financial planning. This includes:

- Budgeting: Creating a detailed budget to track income and expenses, ensuring that mortgage payments are prioritized.

- Automatic Payments: Setting up automatic payments to ensure timely payment each month.

- Emergency Fund: Establishing an emergency fund to cover unexpected expenses and prevent the need to skip mortgage payments.

- Regular Monitoring: Regularly reviewing your bank accounts and mortgage statements to track payments and identify potential issues.

Exploring the Connection Between Payment Timing and Mortgage Grace Periods

The relationship between precise payment timing and the grace period is crucial. While the grace period provides a buffer, it's not an excuse for habitual lateness. Understanding when your payment is due, and when the grace period ends, is essential.

Key Factors to Consider:

Roles and Real-World Examples: Imagine a scenario where your payment is due on the 1st of the month. A 5-day grace period means you have until the 6th to make the payment without incurring late fees. However, consistently paying on the 6th, even though technically within the grace period, is risky. If you have any unexpected interruptions to your income or banking access, this might cause you to miss the payment completely.

Risks and Mitigations: The risks of relying on the grace period are numerous. Over-reliance can lead to the establishment of a pattern of late payments, ultimately causing substantial financial damage and potentially resulting in foreclosure. Mitigation involves establishing a proactive financial plan as previously discussed, coupled with consistent tracking of your payment due date and diligent adherence to it, whenever possible.

Impact and Implications: The cumulative effect of missed payments, even those falling within the grace period, can lead to significant financial difficulties. It not only affects your credit score but also exposes you to potential foreclosure proceedings.

Conclusion: Reinforcing the Connection

The connection between precise payment timing and the grace period is delicate. The grace period is a safety net, not a free pass for lateness. Responsible management requires proactive planning and diligent adherence to payment deadlines.

Further Analysis: Examining Payment Methods in Greater Detail

Different payment methods can affect whether a payment is considered on time, even within the grace period. For example, payments made via mail might take longer to process, increasing the risk of missing the grace period despite sending it before the due date. Electronic payments generally provide faster processing and are safer.

FAQ Section: Answering Common Questions About Mortgage Grace Periods

What is a mortgage grace period? A mortgage grace period is a short time after your payment due date during which you can make your payment without incurring late fees.

How long is a typical grace period? The length of a mortgage grace period varies depending on the lender and loan type, typically ranging from a few days to two weeks.

What happens if I miss my payment, even within the grace period? While late fees might be avoided, the payment is still late and can affect your credit score. Repeated lateness could lead to more serious consequences.

Does my lender have to tell me about the grace period? The grace period details are typically outlined in your mortgage loan agreement. If unsure, consult your lender directly.

Can I negotiate a longer grace period with my lender? This is highly unlikely, but discussing financial difficulties with your lender might open avenues for alternative solutions like forbearance or a loan modification.

Practical Tips: Maximizing the Benefits of Understanding Grace Periods

- Understand the Basics: Know the exact due date and the length of your grace period as stated in your loan documents.

- Set up Automatic Payments: This eliminates the risk of forgetting payments and ensures timely remittance.

- Monitor Your Account: Regularly check your account to ensure payments are processed and credited correctly.

- Communicate with Your Lender: If facing financial difficulties, contact your lender promptly to discuss potential solutions.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your mortgage grace period is essential for responsible homeownership. While it offers a safety net for occasional unforeseen circumstances, relying on it shouldn't become a habit. Proactive financial planning, careful tracking of payment due dates, and prompt communication with your lender are critical for avoiding the potentially severe consequences of missed payments. Remember, the grace period is a privilege, not a right, and should be treated with respect and responsibility.

Latest Posts

Latest Posts

-

How To Learn Investment Management

Apr 06, 2025

-

How To Teach Money Management

Apr 06, 2025

-

How To Learn Finance Management

Apr 06, 2025

-

How To Learn Asset Management

Apr 06, 2025

-

How To Learn Wealth Management

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Is The Grace Period To Pay Mortgage . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.