What Is Good Credit Utilization Rate

adminse

Apr 07, 2025 · 9 min read

Table of Contents

Decoding the Mystery: What is a Good Credit Utilization Rate?

What if your financial future hinges on understanding your credit utilization rate? Mastering this crucial metric can unlock doors to better interest rates, higher credit limits, and ultimately, a stronger financial standing.

Editor’s Note: This article on credit utilization rates was published today and provides up-to-date insights for managing your credit effectively. We’ve consulted leading financial experts and analyzed current industry trends to give you the most accurate and actionable advice.

Why Credit Utilization Matters: Relevance, Practical Applications, and Industry Significance

Credit utilization rate is a fundamental aspect of personal finance often overlooked despite its significant impact on credit scores. It represents the proportion of your available credit you're currently using. Lenders closely monitor this metric because it's a strong indicator of your debt management capabilities. A high utilization rate suggests you're heavily reliant on credit, increasing the perceived risk to lenders. Conversely, a low utilization rate demonstrates responsible credit management, making you a lower-risk borrower. This, in turn, can influence your eligibility for loans, the interest rates offered, and even the credit limits extended to you. Understanding and managing your credit utilization rate is crucial for securing favorable financial terms and building a strong credit history.

Overview: What This Article Covers

This article delves into the core aspects of credit utilization rates, exploring its definition, ideal ranges, the impact on your credit score, strategies for improvement, and the nuances of different credit card accounts. Readers will gain actionable insights, backed by data-driven research and expert analysis, to effectively manage their credit and improve their financial health.

The Research and Effort Behind the Insights

This article is the result of extensive research, incorporating insights from leading financial institutions, credit scoring agencies, and consumer finance experts. Data on credit scoring models and their weighting of utilization rates is referenced to ensure accuracy. The information presented is grounded in evidence-based research and practical applications, providing readers with a trustworthy guide to credit management.

Key Takeaways: Summarize the Most Essential Insights

- Definition and Core Concepts: A comprehensive explanation of credit utilization rate and its calculation.

- Ideal Utilization Rate Ranges: Understanding the recommended percentages for optimal credit health.

- Impact on Credit Scores: How credit utilization affects the three major credit bureaus (Equifax, Experian, and TransUnion).

- Strategies for Improvement: Actionable steps to lower your credit utilization and improve your credit score.

- Nuances of Multiple Credit Cards: Managing utilization across multiple accounts effectively.

- Addressing High Utilization: Solutions for those with already high credit utilization rates.

- The Role of Credit Reports: Understanding how to interpret credit reports and identify areas for improvement.

Smooth Transition to the Core Discussion

With a clear understanding of why credit utilization matters, let's dive deeper into its key aspects, exploring how to calculate it, the ideal ranges, and practical strategies for improvement.

Exploring the Key Aspects of Credit Utilization Rate

1. Definition and Core Concepts:

Credit utilization rate is calculated by dividing your total credit card debt by your total available credit. For example, if you have a total credit limit of $10,000 across all your cards and owe $2,000, your credit utilization rate is 20% ($2,000 / $10,000 = 0.20 or 20%). This is a crucial metric for lenders assessing your creditworthiness. It essentially shows how much of your available credit you're using, providing insight into your spending habits and debt management skills.

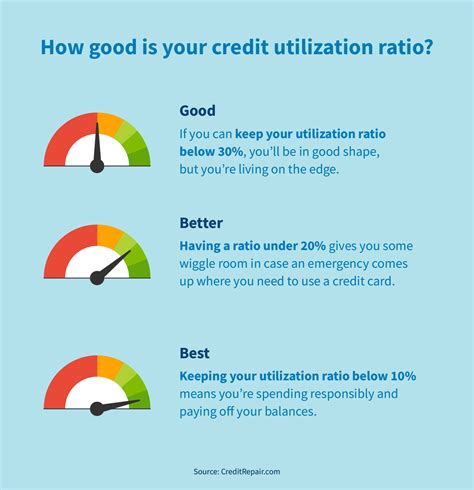

2. Ideal Utilization Rate Ranges:

While there isn't a universally agreed-upon "perfect" number, financial experts generally recommend keeping your credit utilization rate below 30%. Aiming for an even lower rate, ideally below 10%, is often advised for optimal credit health. This demonstrates responsible credit management to lenders and can significantly impact your credit score. A utilization rate consistently below 30% signals to lenders that you’re managing your debt effectively and are less likely to default on payments.

3. Impact on Credit Scores:

Credit utilization rate is a significant factor in your credit score calculations. All three major credit bureaus (Equifax, Experian, and TransUnion) incorporate this metric into their scoring models, though the precise weight might vary slightly. A high utilization rate negatively affects your score, indicating increased risk to lenders. Conversely, a low utilization rate positively impacts your score, reflecting responsible financial behavior. The impact is not linear; exceeding 30% can cause a more substantial drop in your score compared to the incremental improvement seen when going from 10% to 5%.

4. Strategies for Improvement:

Several strategies can help lower your credit utilization rate:

- Pay Down Existing Debt: The most direct approach is to proactively reduce your outstanding balances on credit cards. Prioritize high-interest debt first and consider debt consolidation options if feasible.

- Increase Your Credit Limits: Requesting a credit limit increase from your credit card issuer can lower your utilization rate without necessarily changing your spending habits. However, be mindful of responsible spending even with a higher limit.

- Open a New Credit Card: If your existing credit utilization is high, a new card with a high limit can spread your debt across multiple accounts, effectively lowering your overall utilization rate. Ensure you can manage payments across multiple accounts.

- Avoid Opening Multiple Cards Simultaneously: Applying for multiple cards in a short period can negatively impact your credit score and is not recommended as a strategy to reduce utilization.

- Monitor Your Spending: Track your spending and ensure it aligns with your available credit. Budgeting tools and apps can help in monitoring and managing expenses.

5. Nuances of Multiple Credit Cards:

Managing multiple credit cards requires a more nuanced approach. The overall utilization rate across all your cards is considered by lenders. Even if one card has a low utilization rate, a high rate on another can still negatively impact your overall score. It's essential to monitor and manage the utilization rate of each card individually while keeping a close eye on the aggregated utilization across all your accounts.

6. Addressing High Utilization:

If you already have a high credit utilization rate, immediate action is crucial. Contact your credit card issuers to explore options like increasing your credit limit or negotiating a lower interest rate. Develop a repayment plan that addresses high-interest debt first and commits to consistent payments. Consider seeking professional financial advice if you're struggling to manage your debt.

7. The Role of Credit Reports:

Regularly reviewing your credit reports from all three major bureaus is essential for monitoring your credit utilization rate and identifying any discrepancies or errors. This allows you to proactively address potential issues and maintain a healthy credit profile. You are entitled to a free credit report annually from each bureau.

Closing Insights: Summarizing the Core Discussion

Credit utilization rate is not just a number; it's a crucial indicator of your financial health and responsible credit management. By understanding its impact on your credit score and implementing effective strategies for improvement, you can significantly enhance your financial well-being and unlock better opportunities for borrowing in the future.

Exploring the Connection Between Payment History and Credit Utilization Rate

Payment history is another critical factor influencing your credit score, and it's intricately linked to your credit utilization rate. While they are distinct metrics, they work in tandem to shape your overall creditworthiness.

Key Factors to Consider:

Roles and Real-World Examples: A consistently high credit utilization rate can lead to missed or late payments. When you're using a large portion of your available credit, it can be challenging to manage payments, particularly during unexpected expenses. Conversely, responsible credit usage, reflected in a low utilization rate, creates a buffer that makes it easier to meet payment obligations on time, strengthening your payment history.

Risks and Mitigations: A poor payment history, exacerbated by high credit utilization, can severely damage your credit score. To mitigate this risk, focus on consistently making on-time payments, regardless of your utilization rate. Develop a robust budget to manage expenses and prioritize debt repayment.

Impact and Implications: A strong payment history, coupled with low credit utilization, demonstrates excellent financial responsibility, leading to favorable interest rates, higher credit limits, and easier access to credit products. The opposite scenario can lead to higher interest rates, limited credit access, and even debt collection issues.

Conclusion: Reinforcing the Connection

The interplay between payment history and credit utilization rate underscores the importance of holistic credit management. While a low utilization rate contributes to responsible credit usage, timely payments solidify this impression with lenders, leading to a stronger credit profile and improved financial outcomes.

Further Analysis: Examining Payment History in Greater Detail

Payment history encompasses all your credit accounts and details the consistency of your payments over time. Late payments, missed payments, and defaults are all negatively recorded. The length of your credit history also plays a role; a longer history with consistently on-time payments shows a strong track record of responsible credit use. This underscores the importance of consistently making payments on time and maintaining a healthy credit utilization rate.

FAQ Section: Answering Common Questions About Credit Utilization Rate

Q: What is the worst credit utilization rate?

A: While there isn't a single "worst" number, exceeding 70% or 80% is extremely detrimental and signals significant financial risk to lenders.

Q: Does paying my credit card balance in full each month affect my utilization rate?

A: Yes, paying your balance in full each month minimizes your utilization rate, showing lenders responsible financial management. Even if you use your card heavily, a zero balance at the end of the month keeps your utilization rate at 0%.

Q: How often should I check my credit utilization rate?

A: It's advisable to monitor your credit utilization rate monthly to ensure it remains within the recommended range.

Q: Can I improve my credit score quickly by reducing my credit utilization?

A: Yes, reducing your credit utilization can be a relatively quick way to see a positive impact on your credit score because it's a significant factor in the calculation.

Practical Tips: Maximizing the Benefits of a Low Credit Utilization Rate

-

Set a Budget: Create a realistic budget to track income and expenses, ensuring you stay within your spending limits.

-

Automate Payments: Set up automatic payments to avoid missed payments and maintain a positive payment history.

-

Monitor Your Credit Reports: Regularly review your credit reports from all three bureaus to detect any errors or inconsistencies.

-

Request Credit Limit Increases: If you have a long history of on-time payments, request higher credit limits responsibly to lower your utilization rate.

-

Utilize Budgeting Apps: Employ budgeting apps to track your spending, manage your budget, and stay informed about your credit utilization.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding and managing your credit utilization rate is a fundamental aspect of responsible personal finance. By maintaining a low utilization rate and consistently making on-time payments, you demonstrate responsible credit management to lenders, leading to a stronger credit score, better interest rates, and access to a wider range of financial products. Proactive monitoring and responsible financial practices are essential keys to unlocking the benefits of a healthy credit profile.

Latest Posts

Latest Posts

-

When Does Discover Credit Card Report To Credit Bureau

Apr 08, 2025

-

When Does My Credit Card Report To Credit Bureaus

Apr 08, 2025

-

When Does Chase Credit Card Report To Credit Bureaus

Apr 08, 2025

-

When Does Wells Fargo Credit Card Report To Bureaus

Apr 08, 2025

-

When Do Credit Card Companies Report To Bureaus

Apr 08, 2025

Related Post

Thank you for visiting our website which covers about What Is Good Credit Utilization Rate . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.