What Is A Money Market Account Vs Savings

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Money Market Account vs. Savings Account: Unveiling the Differences

What's the best way to keep your hard-earned money safe and growing, a money market account or a savings account? Choosing between these two popular options requires understanding their key differences, which can significantly impact your financial well-being.

Editor’s Note: This article on money market accounts versus savings accounts was published today, providing readers with the most up-to-date information and insights on these crucial financial tools. We've compared features, benefits, and drawbacks to help you make the right choice for your financial goals.

Why Understanding Money Market and Savings Accounts Matters:

Money market accounts (MMAs) and savings accounts are foundational components of personal finance. They provide safe places to store funds, offering varying levels of accessibility and potential returns. Understanding their differences is critical for optimizing your savings strategy, making informed financial decisions, and potentially maximizing your earnings. These accounts play a crucial role in building emergency funds, saving for future goals (like a down payment or retirement), and managing cash flow effectively. The choice between an MMA and a savings account significantly impacts your financial flexibility and potential earnings over time.

Overview: What This Article Covers:

This article will provide a detailed comparison of money market accounts and savings accounts. We’ll delve into their definitions, features, interest rates, fees, accessibility, and suitability for different financial situations. We will explore the nuances of each account type to help you determine which best aligns with your individual needs and financial objectives.

The Research and Effort Behind the Insights:

This article is the product of extensive research, drawing upon information from reputable financial institutions, regulatory bodies, and expert analyses of the banking and investment sectors. Data on interest rates, fees, and account features were gathered from a range of sources to ensure accuracy and to reflect the current market landscape. The information presented aims to be objective, informative, and relevant to a broad range of readers.

Key Takeaways:

- Definition and Core Concepts: Clear definitions of MMAs and savings accounts, highlighting their fundamental differences.

- Interest Rates and Earnings: A comparison of typical interest rates and potential earnings for each account type.

- Fees and Charges: An examination of the common fees associated with MMAs and savings accounts.

- Accessibility and Liquidity: An analysis of how easily funds can be accessed from each account type.

- FDIC Insurance: An explanation of the federal insurance coverage offered for both account types.

- Suitability for Different Financial Goals: Guidance on which account type is best suited for various financial objectives.

Smooth Transition to the Core Discussion:

With a foundation of understanding the importance of choosing the right account, let's delve into the specific characteristics of money market accounts and savings accounts.

Exploring the Key Aspects of Money Market Accounts (MMAs) and Savings Accounts:

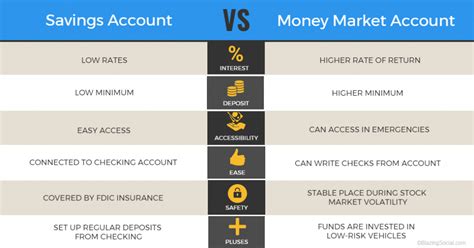

1. Definition and Core Concepts:

A savings account is a basic deposit account offered by banks and credit unions. It's designed primarily for storing money safely and earning a modest interest rate. Funds are readily accessible, typically through ATM withdrawals, debit cards, and online transfers. Savings accounts generally have lower minimum balance requirements than MMAs.

A money market account (MMA) is a type of savings account that offers a slightly higher interest rate than a standard savings account. MMAs often come with additional features, such as check-writing capabilities (although limitations may apply) and debit card access. They usually require a higher minimum balance than savings accounts. MMAs invest in a portfolio of short-term, low-risk securities, which contributes to their higher interest rates.

2. Interest Rates and Earnings:

Interest rates for both MMAs and savings accounts fluctuate based on prevailing market conditions. MMAs typically offer a higher annual percentage yield (APY) than savings accounts. However, the difference is not always substantial. It's crucial to compare APYs from different financial institutions to find the best rates available. The interest earned is generally compounded, meaning interest earned is added to the principal balance, increasing future interest earnings.

3. Fees and Charges:

Both MMAs and savings accounts can incur fees. Common fees include monthly maintenance fees (waived if a minimum balance is maintained), overdraft fees (if the account balance falls below zero), and insufficient funds fees. Some MMAs may charge fees for check writing or other services. It's essential to carefully review the fee schedule of each account before opening it.

4. Accessibility and Liquidity:

Both MMAs and savings accounts offer relatively easy access to funds. Savings accounts usually have fewer limitations on withdrawals. MMAs might have limitations on the number of withdrawals or transfers allowed per month. However, both account types provide convenient access to your money for everyday needs or emergencies.

5. FDIC Insurance:

In the United States, both MMAs and savings accounts offered by FDIC-insured institutions are insured up to $250,000 per depositor, per insured bank, for each account ownership category. This insurance protects your funds in case the financial institution fails.

6. Suitability for Different Financial Goals:

- Emergency Fund: Both MMAs and savings accounts are suitable for building an emergency fund. The ease of access makes them ideal for unexpected expenses.

- Short-Term Savings Goals: For short-term savings goals (e.g., a down payment, vacation), both are appropriate. MMAs might offer slightly better returns.

- Long-Term Savings Goals: While these accounts are not designed for long-term growth, they can serve as a holding place for funds earmarked for future investments. Higher-yield options may be more suitable for long-term growth.

Exploring the Connection Between Interest Rate Fluctuations and MMA/Savings Accounts:

The relationship between interest rate fluctuations and MMA/savings accounts is direct and significant. Interest rates offered on both account types are largely determined by the Federal Reserve's monetary policy and overall market conditions. When interest rates rise, both MMAs and savings accounts typically offer higher APYs. Conversely, when interest rates fall, APYs decrease. Therefore, carefully monitoring interest rates and comparing offers from different institutions is crucial to maximize earnings.

Key Factors to Consider:

- Roles and Real-World Examples: A retiree might prefer an MMA for easy access to funds while maintaining a slightly higher yield. A young adult saving for a down payment might choose a savings account due to lower minimum balance requirements.

- Risks and Mitigations: The primary risk is low interest rates, resulting in minimal earnings. Mitigation involves comparing rates and potentially exploring higher-yield options once savings goals are met.

- Impact and Implications: Changes in interest rates directly impact the earnings potential of both MMA and savings accounts. Understanding this dynamic allows for more informed financial planning.

Conclusion: Reinforcing the Connection:

The interplay between interest rate fluctuations and the choice between an MMA and savings account is pivotal for achieving financial goals. By understanding how interest rates influence earnings and account features, individuals can optimize their savings strategy and maximize the return on their funds.

Further Analysis: Examining Interest Rate Volatility in Greater Detail:

Interest rate volatility can significantly impact returns on MMAs and savings accounts. Periods of high volatility can lead to both increases and decreases in APYs. Tracking economic indicators like inflation and the Federal Reserve's actions can help anticipate potential rate shifts.

FAQ Section: Answering Common Questions About MMAs and Savings Accounts:

Q: What is the main difference between an MMA and a savings account?

A: MMAs generally offer slightly higher interest rates than savings accounts but often require higher minimum balances. MMAs may also offer additional features like check-writing capabilities.

Q: Which account is better for an emergency fund?

A: Both are suitable for emergency funds, prioritizing easy access to funds.

Q: Can I overdraft my MMA or savings account?

A: Yes, you can overdraft both account types, resulting in overdraft fees.

Q: Are both MMAs and savings accounts FDIC-insured?

A: Yes, if they are offered by FDIC-insured institutions.

Practical Tips: Maximizing the Benefits of MMAs and Savings Accounts:

- Shop Around: Compare interest rates and fees from multiple banks and credit unions.

- Meet Minimum Balance Requirements: Avoid monthly maintenance fees by maintaining the required minimum balance.

- Automate Savings: Set up automatic transfers from your checking account to build your savings consistently.

- Monitor Interest Rates: Track changes in interest rates to adjust your savings strategy accordingly.

Final Conclusion: Wrapping Up with Lasting Insights:

Choosing between a money market account and a savings account involves considering individual financial goals, risk tolerance, and the current interest rate environment. By carefully weighing the pros and cons of each account type, individuals can make informed decisions to optimize their savings strategies and build a strong financial foundation. Understanding the nuances of each account enables individuals to effectively manage their finances and achieve their financial aspirations.

Latest Posts

Latest Posts

-

What Credit Score Do You Need For Samsung Credit

Apr 07, 2025

-

What Credit Do You Need For Samsung Financing

Apr 07, 2025

-

What Credit Score Do You Need To Get Samsung Financing

Apr 07, 2025

-

What Is Your Credit Utilization Percentage

Apr 07, 2025

-

What Is Your Credit Utilization Ratio

Apr 07, 2025

Related Post

Thank you for visiting our website which covers about What Is A Money Market Account Vs Savings . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.