What Is A Money Market Account Fidelity

adminse

Apr 05, 2025 · 9 min read

Table of Contents

Unlocking the Potential: What is a Fidelity Money Market Account?

What if securing your savings and accessing your funds easily were seamlessly integrated? Fidelity's money market accounts offer precisely that: a secure, accessible haven for your cash.

Editor’s Note: This article on Fidelity money market accounts was published today, providing readers with the latest information and insights into this valuable financial tool.

Why a Fidelity Money Market Account Matters:

Fidelity, a renowned name in financial services, offers a range of money market accounts designed to help individuals and investors manage their short-term cash needs. These accounts provide a safe place to park funds while earning a competitive interest rate, unlike traditional checking accounts that often offer negligible returns. The relevance stems from their dual functionality: liquidity and growth. They are crucial for emergency funds, short-term investment goals, and bridging the gap between larger investments. Their accessibility and relatively low risk make them an attractive option for a diversified investment portfolio, especially for risk-averse investors.

Overview: What This Article Covers:

This article provides a detailed exploration of Fidelity money market accounts, covering their features, benefits, drawbacks, different account types offered, eligibility criteria, and how they compare to other savings options. Readers will gain a comprehensive understanding of how to choose the right account and effectively manage their short-term funds with Fidelity.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing upon Fidelity's official website, financial news articles, independent financial analyses, and comparisons with similar offerings from other financial institutions. Every piece of information presented is meticulously checked to ensure accuracy and provide readers with reliable guidance.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of Fidelity money market accounts and their underlying principles.

- Account Types and Features: A detailed comparison of different Fidelity money market account options available to investors.

- Interest Rates and Earnings: An analysis of how interest rates are determined and how they compare to other savings vehicles.

- Fees and Minimums: A transparent overview of any associated fees and minimum balance requirements.

- Accessibility and Liquidity: An examination of how easily funds can be accessed and transferred.

- Risk and Security: An assessment of the level of risk involved and the security measures in place to protect funds.

- Comparison with Alternatives: A comparison of Fidelity money market accounts with other savings and investment options.

- Practical Applications and Strategies: Examples of how individuals can use Fidelity money market accounts to achieve their financial goals.

Smooth Transition to the Core Discussion:

Now that the groundwork has been laid, let's delve into the specifics of Fidelity money market accounts, exploring their nuances and practical applications for various financial situations.

Exploring the Key Aspects of Fidelity Money Market Accounts:

1. Definition and Core Concepts:

A Fidelity money market account (MMA) is a type of savings account that invests in low-risk, highly liquid securities, such as Treasury bills, certificates of deposit (CDs), and commercial paper. Unlike traditional savings accounts, MMAs often offer higher interest rates because they invest in a wider range of instruments. The funds are generally FDIC-insured (up to the standard limits) when held within a bank-sponsored Fidelity money market fund. For accounts held within brokerage accounts, the investment is not directly FDIC insured. However, Fidelity employs robust security measures to protect client assets.

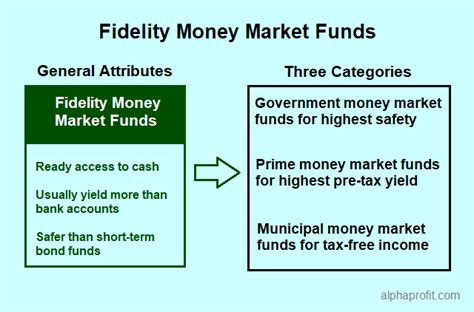

2. Account Types and Features:

Fidelity offers several types of money market accounts, each with varying features and benefits. These might include:

- Cash Management Accounts: These accounts often combine the features of a checking account, savings account, and money market account, providing a centralized hub for managing various financial activities.

- Brokerage-Linked Money Market Funds: These accounts are part of a larger brokerage account and offer access to a wider range of investment options.

- Government Money Market Funds: These funds invest primarily in U.S. government securities, offering a very low-risk option for investors.

The specific features will vary depending on the chosen account type. Some common features include online account access, debit card options (for cash management accounts), and automatic transfers.

3. Interest Rates and Earnings:

Interest rates on Fidelity money market accounts fluctuate based on prevailing market conditions. They are typically higher than those offered by standard savings accounts but lower than those offered by higher-risk investments. The interest is generally compounded daily and credited to the account monthly. It’s crucial to regularly check the current interest rate offered as it’s subject to change.

4. Fees and Minimums:

Fidelity may impose fees depending on the type of money market account chosen. These could include minimum balance requirements, maintenance fees, or fees for certain transactions. It’s vital to carefully review the fee schedule for the specific account you’re considering to avoid unexpected charges.

5. Accessibility and Liquidity:

Fidelity money market accounts provide high liquidity, meaning funds can be accessed quickly and easily. Online transfers, ATM withdrawals (depending on the account type), and check writing options (for suitable accounts) allow for convenient access to your money.

6. Risk and Security:

While considered low-risk, money market accounts are not entirely risk-free. Interest rate fluctuations can impact returns, and while the underlying investments are typically low-risk, there's still a small potential for loss, particularly within brokerage-linked accounts where the fund is not FDIC insured. Fidelity employs robust security measures to protect client assets, but it is important to understand that no investment is entirely without risk.

7. Comparison with Alternatives:

Fidelity money market accounts compare favorably to other savings options in several aspects. Compared to traditional savings accounts, they often offer higher interest rates. Compared to CDs, they offer greater liquidity, though CDs might offer slightly higher returns for longer lock-in periods. Compared to high-yield savings accounts, MMAs potentially offer broader investment options, though high-yield savings accounts often provide a simpler structure.

Exploring the Connection Between FDIC Insurance and Fidelity Money Market Accounts:

The relationship between FDIC insurance and Fidelity money market accounts is crucial to understand. FDIC insurance protects deposits in banks up to a certain limit. However, this insurance only applies directly to accounts held within bank-sponsored money market funds. If you hold a money market fund within a Fidelity brokerage account, the investment itself is not directly FDIC insured. While Fidelity maintains robust security measures and invests in low-risk securities, the lack of direct FDIC insurance warrants careful consideration.

Key Factors to Consider:

- Roles and Real-World Examples: Individuals use Fidelity money market accounts for emergency funds, short-term savings goals, and as a parking spot for funds before investing in other assets. For example, someone saving for a down payment might use a money market account to accumulate funds while earning interest.

- Risks and Mitigations: The main risk is interest rate fluctuation. To mitigate this, investors might diversify their portfolio, incorporating other investment options alongside the money market account.

- Impact and Implications: Choosing the right money market account can significantly impact overall financial returns and security. Careful research and understanding of account features are key.

Conclusion: Reinforcing the Connection:

The interplay between FDIC insurance and the choice of money market account underscores the need for careful due diligence. Understanding the nuances of different Fidelity money market account types, their associated risks, and the absence of direct FDIC insurance for brokerage-linked accounts empowers investors to make informed decisions aligned with their risk tolerance and financial goals.

Further Analysis: Examining FDIC Insurance in Greater Detail:

The FDIC (Federal Deposit Insurance Corporation) is an independent agency of the U.S. government that insures deposits in banks and savings associations. It is crucial to understand that the FDIC does not insure investments in money market funds held through brokerage accounts. These funds are typically insured through the fund itself, relying on the investment strategy and the reputation of the fund manager.

FAQ Section: Answering Common Questions About Fidelity Money Market Accounts:

- What is a Fidelity Money Market Account? A Fidelity money market account is a type of savings account offered by Fidelity Investments that invests in low-risk, short-term debt instruments.

- How is a Fidelity money market account different from a regular savings account? Fidelity MMAs typically offer higher interest rates than standard savings accounts, although the rates fluctuate.

- Is my money safe in a Fidelity money market account? Your money is generally secure, especially within bank-sponsored Fidelity money market funds that are FDIC-insured. However, for brokerage-linked accounts, while Fidelity employs robust security measures, it's not directly FDIC insured.

- How much interest can I earn? The interest rate varies depending on market conditions and the specific account type. It is generally higher than a regular savings account but lower than many other investment vehicles.

- What are the fees associated with a Fidelity money market account? Fidelity may charge fees depending on the account type. Review the fee schedule carefully before opening an account.

- How do I access my money? Access methods vary depending on the account type. Options may include online transfers, ATM withdrawals (for specific accounts), checks, and debit cards.

Practical Tips: Maximizing the Benefits of Fidelity Money Market Accounts:

- Understand the Basics: Thoroughly research the different types of Fidelity money market accounts to find the best fit for your needs and risk tolerance.

- Compare Rates: Regularly compare interest rates offered by Fidelity and other institutions to ensure you're receiving a competitive return.

- Monitor Fees: Carefully review the fee schedule and ensure you understand all associated costs.

- Diversify Investments: Don't rely solely on a money market account for all your savings. Diversification is crucial for managing risk.

- Set Realistic Goals: Use your money market account strategically to achieve specific short-term financial goals.

Final Conclusion: Wrapping Up with Lasting Insights:

Fidelity money market accounts provide a valuable tool for managing short-term funds, offering a balance between liquidity, accessibility, and competitive interest rates. By understanding the nuances of different account types, fees, and the implications of FDIC insurance (or its lack thereof), individuals can leverage these accounts to achieve their financial objectives efficiently and securely. Remember that careful research and planning are crucial for making informed decisions that align with your individual circumstances.

Latest Posts

Latest Posts

-

Money Management Mql4

Apr 06, 2025

-

Money Management Xauusd

Apr 06, 2025

-

Money Management Problem

Apr 06, 2025

-

Tools To Manage Finances

Apr 06, 2025

-

What Are Wealth Management Tools

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Is A Money Market Account Fidelity . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.