What Is A Grace Period For Credit Card Bills

adminse

Apr 02, 2025 · 8 min read

Table of Contents

What happens if I miss a credit card payment? Is there a safety net?

Understanding credit card grace periods is crucial for responsible credit management, offering a buffer against accidental late payments and helping you avoid damaging your credit score.

Editor’s Note: This article on credit card grace periods was published today, providing readers with up-to-date information on this important aspect of credit card management. Understanding your grace period is vital for maintaining a healthy credit profile.

Why Grace Periods Matter: Avoiding Late Fees and Protecting Your Credit

A grace period on a credit card offers a crucial buffer between the end of your billing cycle and the due date of your payment. It's a period where you can pay your statement balance in full without incurring late fees or negative impacts on your credit score. This seemingly small window has significant implications for your financial health and overall creditworthiness. Failing to understand and utilize your grace period can lead to unnecessary expenses, damage your credit rating, and potentially impact your ability to secure loans or other forms of credit in the future. Understanding this period is crucial for responsible financial management and long-term financial success.

Overview: What This Article Covers

This article provides a comprehensive explanation of credit card grace periods, covering their definition, how they work, factors affecting their length, and the potential consequences of missing payments. We'll explore common misconceptions, offer practical tips for managing your payments effectively, and address frequently asked questions. Ultimately, the goal is to empower readers with the knowledge they need to avoid late fees and maintain a healthy credit history.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon information from reputable sources such as the Consumer Financial Protection Bureau (CFPB), leading financial institutions' websites, and consumer finance publications. The information provided reflects current industry standards and practices. The goal is to deliver accurate and up-to-date information to help readers navigate the complexities of credit card grace periods effectively.

Key Takeaways: Summarizing the Most Essential Insights

- Definition and Core Concepts: A clear definition of a credit card grace period and its fundamental principles.

- Grace Period Calculation: Understanding how grace periods are calculated and what factors influence their length.

- Impact of Payments: How various payment methods and amounts affect the grace period.

- Consequences of Missing Payments: Exploring the financial and credit implications of missing a payment during the grace period.

- Strategies for Avoiding Late Payments: Practical tips for effective credit card management and avoiding late fees.

Smooth Transition to the Core Discussion

Now that we understand the importance of grace periods, let's delve into the specifics of how they work and what you need to know to utilize them effectively.

Exploring the Key Aspects of Grace Periods for Credit Card Bills

Definition and Core Concepts:

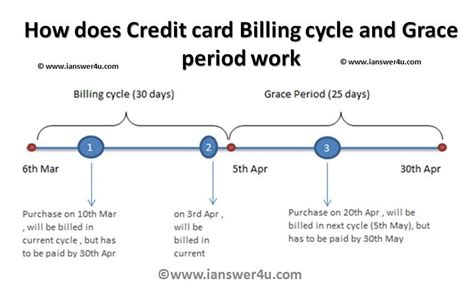

A credit card grace period is the time frame between the end of your billing cycle and the due date of your credit card payment. During this period, you can pay your statement balance in full without incurring any interest charges or late fees. It's a crucial feature designed to give cardholders sufficient time to settle their bills. Importantly, the grace period only applies to the previous month's purchases; any new purchases made during the grace period will begin accruing interest immediately.

How Grace Periods are Calculated:

The grace period typically begins on the date your billing cycle ends. The billing cycle is the period of time between one statement closing date and the next. Your statement will clearly show the closing date and the due date. The number of days between these two dates constitutes your grace period. This is usually between 21 and 25 days, but it can vary depending on your credit card issuer. The due date is prominently displayed on your statement, and it's crucial to pay attention to this date.

Impact of Payments:

The grace period is only applicable if you pay your statement balance in full by the due date. Paying only a portion of your balance, or paying after the due date, negates the grace period. This means that interest will accrue on the entire outstanding balance from the date of the purchase. Different payment methods may have varying processing times, so it’s best to pay well in advance of the due date to avoid any unexpected delays. Online payments, especially through the card issuer's website or app, are generally the fastest and most reliable.

Consequences of Missing Payments:

Missing a credit card payment, even by a single day, has several serious consequences. The most immediate is a late payment fee, which can range from $25 to $39 or more, depending on your credit card issuer. These fees can significantly impact your budget. Furthermore, a missed payment is reported to the major credit bureaus (Equifax, Experian, and TransUnion), negatively impacting your credit score. A lower credit score makes it harder to secure loans, rent an apartment, or even get certain jobs. Repeated missed payments can severely damage your credit, leading to higher interest rates on future loans and difficulty accessing credit altogether.

Strategies for Avoiding Late Payments:

- Set Reminders: Utilize calendar reminders, phone alerts, or budgeting apps to set reminders for your payment due dates.

- Automate Payments: Set up automatic payments from your checking account to ensure timely payments.

- Pay Early: Make your payment a few days before the due date to account for potential processing delays.

- Monitor Your Account: Regularly check your credit card statement and online account to track your balance and due dates.

- Budgeting: Create a budget and allocate sufficient funds to cover your credit card payments.

Exploring the Connection Between Payment Habits and Grace Periods

The relationship between consistent payment habits and effectively utilizing grace periods is undeniably significant. Regular on-time payments demonstrate responsible credit behavior, improving your creditworthiness and potentially leading to better interest rates and credit card offers in the future. Conversely, consistently late payments can damage your credit rating, making future financing more expensive and difficult to obtain.

Key Factors to Consider:

-

Roles and Real-World Examples: Individuals with consistent on-time payments often qualify for better credit terms, including lower interest rates and higher credit limits. Conversely, those with a history of late payments may face higher interest rates and lower credit limits.

-

Risks and Mitigations: The risks associated with late payments include late fees, damage to credit scores, and difficulty securing future credit. Mitigating these risks involves consistently paying on time, budgeting effectively, and setting up automatic payments.

-

Impact and Implications: The impact of consistently missing payments can be far-reaching, affecting various aspects of your financial life, from securing loans and mortgages to obtaining insurance. The implications of late payments can extend far beyond the immediate financial penalties.

Conclusion: Reinforcing the Connection

The connection between consistent on-time payments and the effective use of grace periods is fundamental to maintaining good credit. By utilizing the grace period wisely and establishing a reliable payment history, individuals can strengthen their creditworthiness and secure better financial opportunities in the future.

Further Analysis: Examining the Impact of Credit Utilization

Credit utilization, or the amount of credit you use compared to your total available credit, significantly affects your credit score. High credit utilization, often exceeding 30%, is a negative factor. Maintaining a low credit utilization ratio, ideally below 30%, is crucial for a healthy credit profile. Paying your balance in full before the due date keeps your credit utilization low and reinforces the benefits of the grace period.

FAQ Section: Answering Common Questions About Grace Periods

What is a grace period? A grace period is the time between your statement closing date and the payment due date. It allows you to pay your statement balance without interest.

How long is a grace period? Grace periods typically range from 21 to 25 days, but this varies by issuer. Check your credit card agreement.

What happens if I don't pay my balance by the due date? You'll likely incur late fees and interest will be charged on your outstanding balance. A late payment will also be reported to credit bureaus.

Does the grace period apply to cash advances? No, cash advances generally don't have a grace period, and interest begins accumulating immediately.

Can I still get a grace period if I make a partial payment? No, to get the full benefit of the grace period, you must pay your statement balance in full by the due date.

What if I make my payment on the due date, but it's not processed until the next day? While aiming to pay before the due date is best, most issuers provide a buffer for processing, but check your cardholder agreement to be sure.

Practical Tips: Maximizing the Benefits of Grace Periods

- Understand Your Billing Cycle: Familiarize yourself with your billing cycle and due dates.

- Set Up Payment Reminders: Use technology to avoid missed payments.

- Pay in Full and on Time: Make your payments in full before the due date to avoid interest charges.

- Review Your Statement Carefully: Check for errors and ensure all transactions are accurate.

- Monitor Your Credit Report: Regularly review your credit reports to detect any inaccuracies or issues.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding and effectively utilizing the grace period on your credit card is a cornerstone of responsible credit management. By paying attention to due dates, automating payments when possible, and maintaining a consistent record of on-time payments, you can maximize the benefits of your grace period, protect your credit score, and avoid unnecessary fees. Responsible credit card management not only protects your financial health but also opens doors to better financial opportunities in the future.

Latest Posts

Latest Posts

-

Pcp Payment

Apr 05, 2025

-

Minimum Payment Option Mortgage

Apr 05, 2025

-

Minimum Mortgage Monthly Payment

Apr 05, 2025

-

Mortgage Minimum Amount

Apr 05, 2025

-

Minimum Payment On Mortgage

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is A Grace Period For Credit Card Bills . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.