What Does Total Minimum Payment Due Mean On A Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Unlocking the Mystery: What Does "Total Minimum Payment Due" Really Mean on Your Credit Card?

What if ignoring that seemingly small minimum payment could lead to a cascade of financial difficulties? Understanding your credit card's minimum payment is crucial for maintaining good financial health and avoiding costly mistakes.

Editor’s Note: This article on understanding "Total Minimum Payment Due" on your credit card statement was published today, providing you with up-to-date information to manage your credit responsibly.

Why "Total Minimum Payment Due" Matters: Avoiding the Debt Trap

The seemingly innocuous phrase "Total Minimum Payment Due" holds significant weight in the world of personal finance. It's the bare minimum amount you can pay on your credit card statement each month without incurring late fees. However, relying solely on minimum payments can have severe long-term consequences, leading to escalating debt, higher interest charges, and damage to your credit score. Understanding what this amount comprises and the implications of paying only the minimum is critical for responsible credit card management. This understanding extends beyond simply avoiding late fees; it’s about proactively managing your finances and building a solid credit history.

Overview: What This Article Covers

This comprehensive article delves into the intricacies of the "Total Minimum Payment Due" on your credit card statement. We’ll explore its composition, the implications of consistently paying only the minimum, strategies for avoiding this debt trap, and the long-term effects on your financial well-being. You’ll gain actionable insights backed by clear explanations and practical advice.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing on information from reputable financial institutions, consumer protection agencies, and leading personal finance experts. The information presented is supported by data and analysis, ensuring accuracy and trustworthiness.

Key Takeaways:

- Definition and Core Concepts: A detailed explanation of what constitutes the "Total Minimum Payment Due" and its components.

- Implications of Minimum Payments: The long-term financial consequences of consistently paying only the minimum.

- Strategies for Avoiding the Minimum Payment Trap: Practical steps to manage credit card debt effectively.

- Impact on Credit Score: The correlation between minimum payments and your creditworthiness.

- Calculating the True Cost: Understanding the hidden costs associated with minimum payments.

Smooth Transition to the Core Discussion:

Now that we’ve established the importance of understanding your "Total Minimum Payment Due," let's explore its components and the potential pitfalls of relying on it.

Exploring the Key Aspects of "Total Minimum Payment Due"

1. Definition and Core Concepts:

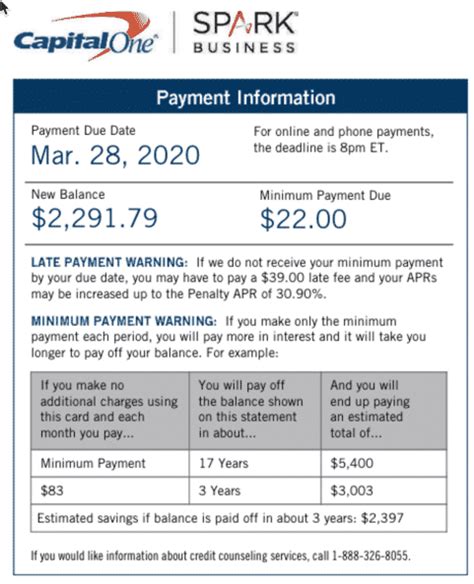

The "Total Minimum Payment Due" is the lowest amount you can pay on your credit card statement by the due date without incurring a late payment fee. This amount typically covers a portion of your current balance, along with any accrued interest and other fees. Crucially, it does not represent the amount necessary to pay off your credit card debt in a timely manner. The minimum payment is usually a small percentage of your outstanding balance (often between 1% and 3%), calculated to keep your account active and avoid immediate penalties.

2. Components of the Minimum Payment:

The minimum payment calculation typically includes:

- Principal: A portion of the original amount you borrowed.

- Interest: The cost of borrowing money, accruing daily on your outstanding balance. This is the most significant component often overlooked.

- Fees: Any additional charges, such as late fees, annual fees, or over-limit fees incurred during the billing cycle.

It's critical to note that the interest calculation is based on the average daily balance of your account throughout the billing cycle. Paying only the minimum payment means a larger portion of your next payment will go towards interest, perpetuating the debt cycle.

3. Applications and Misconceptions:

A common misconception is that paying the minimum payment is a responsible financial strategy. While it avoids immediate penalties, it significantly slows down debt repayment and leads to paying substantially more interest over the long term.

4. Impact on Innovation: (In the context of financial technology)

The rise of financial technology apps and budgeting tools has improved transparency, enabling individuals to monitor their credit card payments more efficiently. These technologies allow for more accurate calculations of total interest paid and projections of debt payoff timelines, helping consumers make informed decisions regarding minimum payment strategies. However, the core principles of interest accumulation and responsible credit management remain the same.

Closing Insights: Summarizing the Core Discussion:

The "Total Minimum Payment Due" is a deceptively simple concept with far-reaching financial implications. Understanding its composition and the pitfalls of relying solely on it is essential for responsible credit management. Paying only the minimum payment delays debt repayment, exponentially increasing the overall cost of credit through prolonged interest accrual.

Exploring the Connection Between High Interest Rates and "Total Minimum Payment Due"

High interest rates significantly influence the effectiveness of minimum payments. With higher interest rates, a larger portion of your minimum payment goes towards interest, leaving a smaller amount to reduce your principal balance. This creates a vicious cycle: the debt remains high, and the interest continues to accumulate.

Key Factors to Consider:

Roles and Real-World Examples: Consider a credit card with a $1,000 balance and a 20% APR. A 2% minimum payment might be $20. Of this, a significant portion goes towards interest, leaving only a small amount to reduce the principal. Over time, the balance remains stubbornly high, and you're paying substantially more than the original $1,000.

Risks and Mitigations: The primary risk is prolonged debt and excessive interest payments. Mitigation strategies include increasing your payments beyond the minimum, exploring debt consolidation options, or seeking professional financial advice.

Impact and Implications: The long-term impact of relying on minimum payments includes damaged credit scores, financial stress, and reduced financial flexibility.

Conclusion: Reinforcing the Connection:

The relationship between high interest rates and the minimum payment due is undeniable. High interest rates exacerbate the already problematic nature of minimum payments, making it crucial to actively work towards reducing debt and minimizing interest charges.

Further Analysis: Examining Interest Calculation in Greater Detail

The interest calculation on your credit card is typically based on your average daily balance. This means interest accrues daily on the outstanding balance, increasing the cost of carrying the debt. Understanding this compounding effect is essential for appreciating the long-term financial implications of minimum payments. Many credit card companies utilize different methods for calculating interest, so reviewing your card's agreement is essential.

FAQ Section: Answering Common Questions About "Total Minimum Payment Due"

Q: What happens if I only pay the minimum payment? You'll avoid late fees, but you'll pay significantly more in interest over time, prolonging debt repayment.

Q: How is the minimum payment calculated? It's usually a percentage of your outstanding balance (often 1-3%), including interest and fees.

Q: Can I negotiate a lower minimum payment? It's unlikely, but you can explore debt management options with the credit card company or a credit counseling agency.

Q: Will paying only the minimum affect my credit score? While not an immediate impact, consistently making only minimum payments signals poor credit management and will negatively impact your credit score over time.

Q: What is the best way to manage my credit card debt? Develop a budget, pay more than the minimum payment each month, and consider debt consolidation or balance transfer options if necessary.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Management

- Create a Budget: Track your income and expenses to understand your spending habits and identify areas where you can save.

- Pay More Than the Minimum: Aim to pay at least double the minimum payment each month to accelerate debt repayment.

- Prioritize High-Interest Debt: Focus on paying down credit cards with the highest interest rates first.

- Consider Debt Consolidation: Explore options to consolidate high-interest debt into a lower-interest loan.

- Seek Professional Help: Contact a credit counselor or financial advisor if you're struggling to manage your debt.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the "Total Minimum Payment Due" is not just about avoiding late fees; it's about understanding the long-term financial implications of your credit card usage. By adopting a proactive approach, diligently managing expenses, and making informed payment decisions, you can avoid the trap of minimum payments and build a strong financial foundation. Ignoring the true cost of minimum payments can lead to significant financial hardship. Take control of your finances today.

Latest Posts

Latest Posts

-

How To Apply For Navy Federal Credit Union

Apr 06, 2025

-

Which Credit Cards Give The Highest Credit Limits

Apr 06, 2025

-

What Card Has The Highest Credit Limit

Apr 06, 2025

-

What Is The Highest Credit Limit For Capital One Gold Mastercard

Apr 06, 2025

-

What Is The Highest Credit Limit You Can Get On A Credit Card

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Does Total Minimum Payment Due Mean On A Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.