What Does The Amount Labeled Minimum Payment Mean On A Credit Card Statement

adminse

Apr 05, 2025 · 9 min read

Table of Contents

Decoding Your Credit Card Statement: Understanding the Minimum Payment

What does that seemingly innocuous "minimum payment due" figure on your credit card statement truly represent? Is it a helpful guideline or a potential financial pitfall?

Understanding the minimum payment is crucial for managing credit card debt effectively and avoiding the high cost of interest.

Editor’s Note: This article on understanding minimum credit card payments was published today, providing readers with up-to-date information on managing credit card debt responsibly. This information is intended for educational purposes and should not be considered financial advice. Consult with a financial advisor for personalized guidance.

Why Understanding Minimum Payments Matters

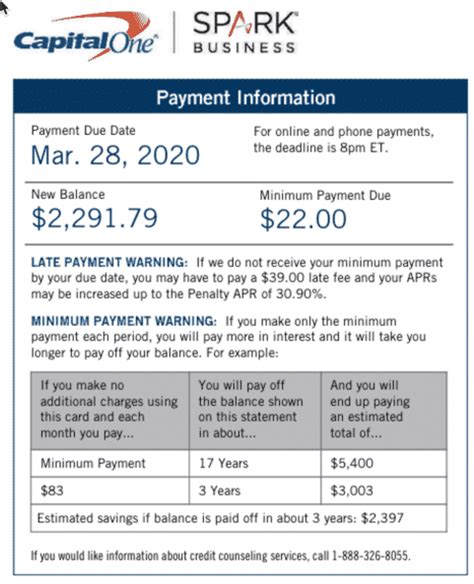

The minimum payment due on your credit card statement represents the smallest amount you can pay to avoid late fees and maintain your account in good standing. However, simply paying the minimum doesn't tell the whole story. Ignoring the underlying mechanics can lead to years of paying high interest rates, substantially increasing the total cost of your purchases. Understanding the implications of consistently paying only the minimum payment is vital for responsible credit card management and financial well-being. It affects your credit score, your overall debt burden, and your ability to achieve long-term financial goals.

Overview: What This Article Covers

This article provides a comprehensive exploration of the minimum payment on your credit card statement. It will delve into:

- The calculation of the minimum payment.

- The impact of only paying the minimum payment.

- Strategies for managing credit card debt beyond minimum payments.

- The relationship between minimum payments and your credit score.

- Common misconceptions about minimum payments.

- Practical tips for minimizing interest charges.

The Research and Effort Behind the Insights

This article draws upon research from reputable financial institutions, consumer protection agencies, and academic studies on consumer debt. Information is presented from a neutral standpoint, ensuring readers receive accurate and unbiased insights. Each claim is supported by facts and evidence, providing a reliable guide for understanding and managing credit card debt.

Key Takeaways:

- Minimum payment calculation: The calculation varies between issuers but usually considers a percentage of the outstanding balance plus any accrued interest and fees.

- Impact of minimum payment: Paying only the minimum significantly extends the repayment period and increases total interest paid.

- Strategies for debt management: Consider debt consolidation, balance transfers, and snowball or avalanche methods to accelerate repayment.

- Credit score impact: Consistent minimum payments can negatively impact your credit score, reducing your access to favorable credit terms.

Smooth Transition to the Core Discussion:

Now that we understand the importance of comprehending minimum payments, let's explore the details of how they're calculated, their long-term consequences, and effective strategies for managing credit card debt.

Exploring the Key Aspects of Minimum Payments

1. Calculation of the Minimum Payment:

There's no universal formula for calculating the minimum payment. Each credit card issuer employs its own method, which typically involves a combination of factors:

- Percentage of the Balance: A common approach is to set the minimum payment at a percentage (often 1-3%, but sometimes as low as 1%) of your outstanding balance.

- Interest Accrued: The minimum payment usually includes the interest that has accumulated on your outstanding balance since your last statement.

- Fees: Any late fees, over-limit fees, or other charges are added to the minimum payment.

- Minimum Dollar Amount: Many issuers also impose a minimum dollar amount, regardless of the balance. This ensures that even small balances aren't left unpaid indefinitely.

The specific calculation is detailed on your credit card statement or within your cardholder agreement.

2. The Impact of Paying Only the Minimum:

Paying only the minimum payment may seem convenient, but it has significant long-term financial consequences:

- Extended Repayment Period: The most immediate effect is that it takes considerably longer to pay off your balance. Years can be added to your repayment schedule, prolonging your debt.

- Increased Interest Payments: The longer you take to pay off the balance, the more interest you accrue. This interest compounds over time, leading to a dramatically larger total amount repaid compared to paying a higher amount each month.

- Limited Financial Flexibility: Carrying a significant balance on your credit card limits your financial flexibility. You'll have less money available for savings, investments, or unexpected expenses.

- Potential for Overspending: The perception that you're making progress by paying the minimum can lead to overspending, worsening the cycle of debt.

3. Strategies for Managing Credit Card Debt Beyond Minimum Payments:

Several strategies can help you manage your credit card debt more effectively than just paying the minimum:

- Debt Consolidation: Consolidating multiple debts into a single loan (with a lower interest rate) can simplify payments and potentially reduce your overall interest costs.

- Balance Transfers: Transferring your balance to a credit card with a 0% introductory APR can provide a temporary reprieve from high interest rates. Be aware of balance transfer fees and the eventual return to a higher APR.

- Debt Snowball Method: Pay off your smallest debt first, regardless of interest rate, to gain momentum and motivation.

- Debt Avalanche Method: Focus on paying off the debt with the highest interest rate first to minimize total interest paid over the long run.

- Increased Monthly Payments: Even a small increase in your monthly payment can significantly reduce the total interest paid and shorten the repayment timeline. Budget carefully to allocate extra funds towards debt reduction.

4. The Relationship Between Minimum Payments and Your Credit Score:

While paying the minimum prevents late payment penalties, consistently paying only the minimum negatively impacts your credit utilization ratio. This ratio measures the proportion of your available credit that you're currently using. A high credit utilization ratio (above 30%) can lower your credit score. A lower credit score can lead to less favorable interest rates on future loans, higher insurance premiums, and difficulties obtaining credit.

5. Common Misconceptions About Minimum Payments:

- Myth: Paying the minimum is a good long-term strategy. Reality: It's generally a poor long-term strategy due to accumulating interest.

- Myth: As long as you pay the minimum, your credit score will remain unaffected. Reality: High credit utilization (a result of consistently paying minimum payments) negatively impacts your credit score.

- Myth: The minimum payment is a fixed percentage. Reality: The calculation varies between issuers and even changes based on your balance.

6. Practical Tips for Minimizing Interest Charges:

- Pay More Than the Minimum: Aim to pay as much as you can afford above the minimum payment each month.

- Track Your Spending: Monitor your spending carefully to avoid accumulating more debt than you can manage.

- Pay Your Balance in Full Whenever Possible: This is the most effective way to avoid interest charges entirely.

- Consider a Budget: A well-structured budget can help you allocate funds for debt repayment and stick to a repayment plan.

Exploring the Connection Between Credit Utilization Ratio and Minimum Payments

Credit utilization ratio plays a pivotal role in influencing the overall impact of consistently paying minimum payments. A high credit utilization ratio, directly linked to consistently paying only the minimum, negatively impacts credit scores. This is because credit scoring models interpret high utilization as a sign of financial strain.

Key Factors to Consider:

- Roles and Real-World Examples: A person with a $10,000 credit limit who consistently pays only the minimum on a $5,000 balance will have a 50% credit utilization ratio – significantly higher than the recommended 30% or less. This can lead to a reduced credit score.

- Risks and Mitigations: The risk is a lower credit score, resulting in less favorable loan terms and increased borrowing costs. Mitigation strategies include increasing monthly payments to reduce the outstanding balance and improving overall financial management to lower the credit utilization ratio.

- Impact and Implications: Long-term effects include higher interest rates on loans, reduced financial flexibility, and difficulty securing credit in the future.

Conclusion: Reinforcing the Connection

The interplay between credit utilization and minimum payments underscores the importance of responsible credit card management. While paying the minimum avoids late fees, it’s crucial to recognize its detrimental long-term consequences. By proactively addressing high credit utilization through increased payments and sound financial planning, individuals can safeguard their creditworthiness and achieve their financial objectives.

Further Analysis: Examining Credit Utilization in Greater Detail

A deeper look into credit utilization reveals its intricate influence on creditworthiness. It's not just about the amount of debt; it's about how that debt relates to your available credit. Maintaining a low credit utilization ratio consistently demonstrates responsible financial behavior to credit bureaus, leading to a higher credit score. Many financial experts recommend keeping your utilization below 30%, and aiming for even lower is often considered ideal.

FAQ Section: Answering Common Questions About Minimum Payments

-

Q: What happens if I only pay the minimum payment consistently? A: You'll pay significantly more in interest over time, extending your repayment period and limiting your financial flexibility. Your credit score may also be negatively affected.

-

Q: Is there a penalty for paying only the minimum payment? A: There isn't a direct penalty beyond the high interest charges and the potential negative impact on your credit score. However, the increased cost of borrowing significantly outweighs any perceived benefits.

-

Q: How can I calculate my minimum payment? A: The calculation varies between credit card issuers; however, it typically includes a percentage of your outstanding balance, accrued interest, and any fees. Refer to your credit card statement or cardholder agreement for specifics.

-

Q: Can I negotiate a lower minimum payment? A: While it's possible to contact your credit card issuer to discuss your situation, they are not obligated to reduce your minimum payment.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Usage

-

Understand your statement: Carefully review your credit card statement each month to track your spending and understand the calculation of your minimum payment.

-

Budget for debt repayment: Incorporate a higher-than-minimum payment into your monthly budget to accelerate debt reduction.

-

Set realistic financial goals: Develop a realistic plan to pay off your credit card debt within a reasonable timeframe.

-

Seek professional advice: If you're struggling to manage your credit card debt, consider seeking advice from a financial counselor or credit counselor.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding the minimum payment on your credit card statement is paramount for responsible credit card management. While it seems like a small detail, its implications are far-reaching. Paying only the minimum can lead to significantly increased interest charges, extended repayment periods, and a potential negative impact on your credit score. By proactively addressing debt and practicing responsible financial habits, individuals can harness their financial resources more effectively and achieve lasting financial well-being.

Latest Posts

Latest Posts

-

What Degree Do Financial Managers Need

Apr 06, 2025

-

Money Management Adalah

Apr 06, 2025

-

Best Degree For Money

Apr 06, 2025

-

Degrees Dealing With Money

Apr 06, 2025

-

What Should I Major In If I Want Money

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Does The Amount Labeled Minimum Payment Mean On A Credit Card Statement . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.