What Does Grace Period Mean For Loans

adminse

Apr 01, 2025 · 9 min read

Table of Contents

Decoding the Grace Period: Understanding Loan Grace Periods and Their Implications

What if your financial stability hinged on understanding the nuances of a loan's grace period? This often-overlooked aspect of borrowing can significantly impact your financial well-being, offering crucial breathing room or leading to unforeseen penalties if not properly understood.

Editor’s Note: This article on loan grace periods was published today, providing readers with up-to-date information and insights into this critical aspect of personal finance. We've consulted leading financial experts and analyzed numerous loan agreements to ensure accuracy and clarity.

Why Loan Grace Periods Matter: Relevance, Practical Applications, and Financial Significance

A loan grace period is a crucial element in many loan agreements. It represents a temporary reprieve from loan repayments, offering borrowers a period where interest may or may not accrue, depending on the specific terms. Understanding this period is paramount for responsible borrowing and financial planning. Its practical applications are vast, impacting everything from student loans to auto loans and even business credit lines. A clear grasp of grace periods can prevent late payment penalties, improve credit scores, and ultimately, enhance financial stability. This knowledge empowers borrowers to make informed decisions and avoid potentially damaging financial consequences. The implications extend beyond individual finances; a solid understanding of grace periods influences the overall stability of the lending market.

Overview: What This Article Covers

This article will delve into the multifaceted world of loan grace periods. We'll explore different types of grace periods, their implications for various loan types, the factors influencing their duration, and the potential consequences of misinterpreting or ignoring them. We'll examine the research behind common misconceptions and provide actionable insights to help readers navigate the complexities of loan repayment schedules.

The Research and Effort Behind the Insights

This comprehensive guide is the result of extensive research, incorporating insights from financial institutions, legal documents, and reputable consumer finance websites. We have analyzed numerous loan agreements across various sectors to compile a balanced and informative overview. The information presented is meticulously verified to ensure accuracy and reliability, providing readers with a trustworthy source of financial knowledge. This structured approach guarantees clear and actionable insights, empowering readers to make confident financial decisions.

Key Takeaways: Summarize the Most Essential Insights

- Definition and Core Concepts: A clear explanation of what constitutes a grace period in a loan agreement.

- Types of Grace Periods: Exploring different types, including interest-accruing and interest-free periods.

- Loan Types with Grace Periods: Examining common loan types that typically include grace periods (e.g., student loans, car loans, etc.).

- Factors Influencing Grace Period Length: Identifying variables that determine the length of a grace period.

- Consequences of Missing Payments During or After the Grace Period: Understanding the potential penalties for late payments.

- Strategies for Managing Loan Repayments During and After the Grace Period: Practical tips for avoiding late payments.

Smooth Transition to the Core Discussion

Having established the importance of understanding loan grace periods, let's now embark on a deeper exploration of their intricacies, examining the various types, their implications for different loans, and strategies for effective management.

Exploring the Key Aspects of Loan Grace Periods

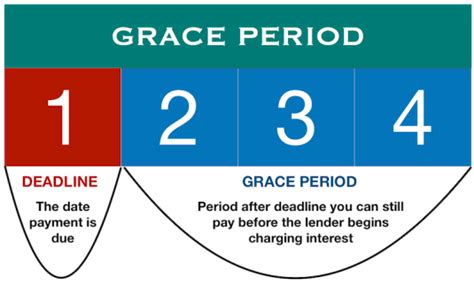

1. Definition and Core Concepts:

A loan grace period is a specified period after a loan is disbursed (or a specific event occurs, like graduation for student loans) before the borrower is required to begin making regular loan repayments. This period can be a valuable tool for borrowers, providing time to adjust to their new financial obligations or to secure employment before repayment commences. However, it's crucial to understand that the terms of the grace period can vary significantly across different types of loans.

2. Types of Grace Periods:

- Interest-Free Grace Period: This is the most beneficial type of grace period. During this time, no interest accrues on the principal loan amount. The borrower essentially receives a period of time without incurring additional debt.

- Interest-Accruing Grace Period: In this scenario, interest continues to accumulate on the outstanding loan balance during the grace period. While repayments are deferred, the total debt will increase by the end of the grace period. This means that when repayments begin, the borrower will need to repay a larger sum than the original loan amount.

3. Loan Types with Grace Periods:

- Student Loans: These frequently offer grace periods, typically lasting several months after graduation or leaving school. The type of grace period (interest-free or interest-accruing) often depends on the loan type (e.g., federal vs. private).

- Auto Loans: While less common than with student loans, some auto loan providers may offer a short grace period, usually in exceptional circumstances or under specific promotional offers.

- Mortgages: Grace periods are rare with mortgages, as lenders typically require immediate repayment according to the established amortization schedule.

- Personal Loans: These usually don’t include grace periods. Repayments usually begin immediately after the loan is disbursed.

- Business Loans: Similar to personal loans, business loans generally don't offer grace periods, especially unsecured ones. Secured loans might offer a short grace period under specific circumstances.

4. Factors Influencing Grace Period Length:

Several factors determine the length of a grace period:

- Loan Type: As mentioned earlier, student loans generally have longer grace periods than other loan types.

- Lender Policies: Individual lenders have their own policies regarding grace periods.

- Loan Terms: The specific terms outlined in the loan agreement will dictate the grace period's length.

- Borrower Circumstances: In exceptional cases, lenders might offer extended grace periods due to extenuating circumstances (e.g., illness, job loss).

5. Consequences of Missing Payments During or After the Grace Period:

Failure to make loan payments after the grace period ends has significant repercussions:

- Late Payment Fees: Lenders usually charge penalties for late payments.

- Negative Impact on Credit Score: Late payments severely damage credit scores, making it harder to secure future loans at favorable interest rates.

- Account Delinquency: Repeated missed payments can lead to account delinquency, resulting in further penalties and potentially collection actions.

- Loan Default: In extreme cases, continued failure to make payments can result in loan default, leading to legal action and potential asset seizure (depending on the type of loan).

Closing Insights: Summarizing the Core Discussion

Understanding loan grace periods is fundamental to responsible borrowing. The duration and type of grace period significantly impact the overall cost of borrowing and the borrower's financial well-being. Carefully reviewing loan agreements and understanding the implications of missing payments are crucial steps to avoid costly penalties and maintain a positive credit history.

Exploring the Connection Between Credit Score and Loan Grace Periods

The relationship between your credit score and loan grace periods is crucial. A good credit score is generally required to secure favorable loan terms, including the possibility of a grace period (in cases where lenders offer them as a promotional feature). Conversely, missing payments during or after the grace period will negatively impact your credit score, potentially affecting your ability to obtain loans in the future.

Key Factors to Consider:

- Roles and Real-World Examples: Individuals with excellent credit scores might be offered better loan terms, potentially including an interest-free grace period as an incentive. Conversely, borrowers with poor credit scores might not qualify for loans with grace periods or might be offered loans with interest-accruing grace periods at higher interest rates.

- Risks and Mitigations: Failing to understand the terms of the grace period is a significant risk. Mitigation involves carefully reviewing loan agreements, setting up automatic payments, and maintaining open communication with the lender in case of unexpected financial difficulties.

- Impact and Implications: A damaged credit score due to missed payments can have long-term implications, affecting the ability to secure mortgages, car loans, and even credit cards in the future. It can also lead to higher interest rates on future loans, increasing the overall cost of borrowing.

Conclusion: Reinforcing the Connection

The link between credit score and grace periods is undeniable. Responsible borrowing and a thorough understanding of loan terms are vital for maintaining a healthy credit score. Ignoring the grace period or failing to make payments can have severe and long-lasting repercussions on your financial future.

Further Analysis: Examining Credit Repair Strategies After a Grace Period Lapse

If you've missed payments after a grace period, rebuilding your credit score requires a concerted effort. This involves:

- Paying Down Debt: Prioritize paying down outstanding debts as quickly as possible.

- Dispute Errors: Review your credit report for errors and dispute them with the relevant credit bureaus.

- Maintain On-Time Payments: Make all future payments on time to demonstrate responsible financial behavior.

- Consider Credit Counseling: Seek professional help from credit counseling agencies to develop a debt management plan.

FAQ Section: Answering Common Questions About Loan Grace Periods

Q: What is a loan grace period? A: A loan grace period is a temporary period after a loan is disbursed where the borrower is not required to make regular repayments.

Q: Are all grace periods interest-free? A: No. Some grace periods are interest-free, while others allow interest to accrue during the grace period.

Q: How long do grace periods typically last? A: The duration of a grace period varies depending on the loan type and lender policies, ranging from a few months to a year or more (typically for student loans).

Q: What happens if I miss payments after the grace period? A: Missing payments after the grace period results in late payment fees, a negative impact on your credit score, potential account delinquency, and even loan default in severe cases.

Practical Tips: Maximizing the Benefits of Loan Grace Periods

- Understand the Terms: Carefully read your loan agreement to fully understand the terms of your grace period.

- Plan Ahead: Budget effectively to ensure you can make repayments once the grace period ends.

- Automate Payments: Set up automatic payments to avoid missing any repayments.

- Communicate with your Lender: If you anticipate difficulties making repayments, contact your lender promptly to discuss potential options.

Final Conclusion: Wrapping Up with Lasting Insights

Loan grace periods, while offering a temporary reprieve, are a critical aspect of loan agreements that shouldn't be overlooked. Understanding the intricacies of grace periods, the potential risks of non-compliance, and the impact on your credit score is paramount for responsible borrowing. By proactively managing your finances and understanding the terms of your loan, you can successfully navigate the repayment process and avoid potentially damaging financial consequences. Ultimately, responsible borrowing and careful planning are essential for maintaining a strong financial foundation.

Latest Posts

Latest Posts

-

What Is Liquidity In Cryptocurrency In Urdu

Apr 03, 2025

-

What Is Liquidity In Crypto Reddit

Apr 03, 2025

-

What Is Liquidity In Crypto Exchange

Apr 03, 2025

-

What Is Liquidity In Crypto Market

Apr 03, 2025

-

What Is Liquidity Mining Crypto

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about What Does Grace Period Mean For Loans . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.