Minimum Payment On Loan

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Unlocking the Secrets of Minimum Loan Payments: A Comprehensive Guide

What if understanding your minimum loan payment could save you thousands of dollars and years of debt? Mastering this seemingly simple concept is crucial for financial health and achieving your long-term goals.

Editor’s Note: This article on minimum loan payments was published today, providing up-to-date information and practical strategies for managing your debt effectively. We aim to demystify this crucial aspect of personal finance and empower you to make informed decisions.

Why Minimum Loan Payments Matter: Relevance, Practical Applications, and Industry Significance

Minimum loan payments are the cornerstone of debt management. Understanding them isn’t just about avoiding late fees; it's about building a solid financial foundation. The implications extend beyond individual finances, impacting broader economic trends and influencing consumer behavior. Ignoring the intricacies of minimum payments can lead to extended debt periods, higher overall interest paid, and significant financial strain. Conversely, a strategic approach to minimum payments can pave the way for faster debt repayment and improved credit scores. This knowledge is vital for navigating the complexities of personal loans, mortgages, credit cards, and student loans.

Overview: What This Article Covers

This article will delve into the core aspects of minimum loan payments, examining their calculation, implications, advantages and disadvantages, and the potential pitfalls of relying solely on them. We will explore strategies for optimizing your repayment plan and offer actionable advice to improve your financial well-being. Readers will gain a comprehensive understanding of minimum payments, empowering them to make informed decisions and achieve their financial objectives.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon reputable financial sources, government publications, and expert analyses in the field of personal finance. The information presented is grounded in established financial principles and aims to provide clear, actionable insights supported by evidence.

Key Takeaways: Summarize the Most Essential Insights

- Understanding Minimum Payment Calculation: Learn how lenders calculate minimum payments and the factors that influence them.

- The High Cost of Minimum Payments: Discover the long-term financial consequences of only paying the minimum.

- Strategies for Accelerated Repayment: Explore effective methods to pay off debt faster and save money on interest.

- The Role of Minimum Payments in Credit Scores: Understand how timely minimum payments affect your creditworthiness.

- Navigating Different Loan Types: Learn how minimum payment calculations vary across different loan products.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding minimum loan payments, let's delve into the details, exploring the mechanics, the implications, and the strategies for effective debt management.

Exploring the Key Aspects of Minimum Loan Payments

1. Definition and Core Concepts:

A minimum loan payment is the smallest amount a borrower is required to pay on a loan each month to remain in good standing with the lender. This amount typically covers a portion of the principal (the original loan amount) and the accrued interest. Failure to meet the minimum payment can result in late fees, damage to credit scores, and potential loan default. The calculation of the minimum payment varies depending on the type of loan.

2. Applications Across Industries:

Minimum payments are a standard feature across various loan products:

- Credit Cards: Credit card minimum payments are usually a small percentage of the outstanding balance (often 1-3%), plus any accrued interest and fees.

- Mortgages: Mortgage minimum payments are typically fixed monthly amounts calculated based on the loan amount, interest rate, and loan term.

- Personal Loans: Similar to mortgages, personal loan minimum payments are usually fixed monthly amounts.

- Student Loans: Student loan minimum payments can vary depending on the type of loan (federal or private) and the repayment plan chosen.

3. Challenges and Solutions:

The primary challenge associated with minimum payments is the long repayment period and the high total interest paid over the life of the loan. Relying solely on minimum payments can trap borrowers in a cycle of debt.

- Solution: Develop a budget to identify extra funds that can be allocated towards accelerated debt repayment. Consider debt consolidation or balance transfer options to potentially lower interest rates. Explore strategies like the debt snowball or debt avalanche methods to prioritize debt repayment.

4. Impact on Innovation:

Financial technology (Fintech) is driving innovation in debt management. Numerous apps and online tools provide budgeting assistance, debt tracking, and automated repayment scheduling, making it easier for borrowers to manage their minimum payments and accelerate repayment.

Closing Insights: Summarizing the Core Discussion

Minimum loan payments are a double-edged sword. While they provide a manageable entry point into debt repayment, relying solely on them can lead to significantly increased costs and extended debt periods. A proactive and informed approach, incorporating budgeting, debt management strategies, and the utilization of available financial tools, is essential for achieving financial freedom.

Exploring the Connection Between Interest Rates and Minimum Loan Payments

The relationship between interest rates and minimum loan payments is paramount. Higher interest rates lead to larger interest components within the minimum payment, leaving less applied towards the principal. This slows down the repayment process, resulting in significantly more interest paid over the life of the loan.

Key Factors to Consider:

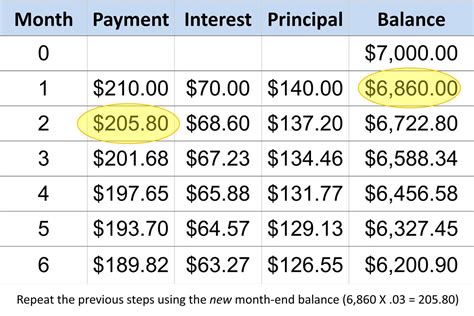

- Roles and Real-World Examples: A $10,000 loan with a 5% interest rate will have a lower minimum payment than the same loan with a 10% interest rate. The higher interest rate results in a larger proportion of the minimum payment going towards interest, leaving less to reduce the principal.

- Risks and Mitigations: High interest rates increase the risk of long-term debt and higher total repayment costs. Mitigation strategies include refinancing to lower interest rates, paying more than the minimum payment each month, and negotiating with lenders for better terms.

- Impact and Implications: High interest rates significantly impact the overall cost of borrowing and can substantially affect a borrower's long-term financial health. Understanding the connection between interest rates and minimum payments is critical for making sound financial decisions.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum loan payments is undeniable. By understanding this relationship and employing effective debt management strategies, borrowers can minimize the impact of high interest rates and accelerate their journey towards debt freedom.

Further Analysis: Examining Interest Rate Fluctuations in Greater Detail

Interest rates are dynamic; they fluctuate based on various economic factors. These fluctuations directly impact minimum payments and the overall cost of borrowing. Understanding these trends can help borrowers anticipate changes and adapt their repayment strategies accordingly. For example, periods of low interest rates present an opportune time for refinancing loans to reduce minimum payments and accelerate debt repayment.

FAQ Section: Answering Common Questions About Minimum Loan Payments

Q: What happens if I only make minimum payments?

A: While you'll avoid immediate delinquency, you'll pay significantly more in interest over the life of the loan, extending the repayment period considerably.

Q: Can I change my minimum payment amount?

A: You generally can't lower your minimum payment; however, you can always pay more than the minimum. This will significantly reduce the overall time and cost of repayment.

Q: What if I miss a minimum payment?

A: Missing a minimum payment can lead to late fees, damage to your credit score, and potentially, loan default.

Practical Tips: Maximizing the Benefits of Minimum Loan Payments (While Minimizing the Drawbacks)

- Understand the Basics: Thoroughly review your loan agreement to understand the calculation of your minimum payment and the terms of your loan.

- Budget Effectively: Create a detailed budget to identify extra funds that can be allocated toward additional principal payments.

- Automate Payments: Set up automatic payments to ensure consistent and timely payments, avoiding late fees.

- Explore Refinancing Options: Explore refinancing opportunities to potentially lower interest rates and reduce your minimum payments.

- Consider Debt Consolidation: Consolidate multiple debts into a single loan with a potentially lower interest rate and a simplified payment schedule.

- Seek Professional Advice: If struggling with debt, consider consulting a financial advisor for personalized guidance.

Final Conclusion: Wrapping Up with Lasting Insights

Minimum loan payments are a fundamental aspect of personal finance, yet often misunderstood. By grasping their intricacies, strategically managing debt, and employing the practical strategies outlined above, individuals can significantly improve their financial health and pave the way for a more secure financial future. Understanding your minimum payment is not just about meeting a requirement; it’s about taking control of your financial destiny.

Latest Posts

Latest Posts

-

What Is The Best Money Management App For Iphone

Apr 06, 2025

-

Money Management Book

Apr 06, 2025

-

Best Money Books To Read

Apr 06, 2025

-

Best Money Books

Apr 06, 2025

-

Good Books On Money Management

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Minimum Payment On Loan . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.