Minimum Payment On 600 Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Payment on a $600 Credit Card: A Comprehensive Guide

What if the seemingly innocuous minimum payment on your $600 credit card could lead to a debt trap? Understanding this crucial aspect of credit card management is key to financial freedom.

Editor’s Note: This article on minimum payments for a $600 credit card balance was published today, providing up-to-date information and insights to help you manage your credit card debt effectively.

Why Minimum Payments Matter: A $600 Balance and Beyond

Many consumers view the minimum payment on their credit card as a convenient option, especially when facing temporary financial strain. However, consistently paying only the minimum on a $600 balance – or any balance for that matter – can have significant long-term financial consequences. It’s not just about the interest; it's about the snowball effect of compounding interest and the extended repayment period, ultimately costing you significantly more money than if you were to repay the debt more aggressively. This impacts your credit score, financial health, and overall peace of mind. The relevance extends beyond the immediate $600; the principles apply to managing any credit card debt.

Overview: What This Article Covers

This comprehensive guide delves into the intricacies of minimum payments on a $600 credit card balance. We’ll explore how minimum payments are calculated, the dangers of only paying the minimum, strategies for accelerating debt repayment, and how to avoid falling into the debt trap. You will gain actionable insights backed by research and practical examples, empowering you to make informed financial decisions.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing on information from reputable financial websites, consumer protection agencies, and analysis of credit card agreements. The goal is to provide clear, accurate, and actionable advice based on established financial principles.

Key Takeaways:

- Understanding Minimum Payment Calculations: How is the minimum payment determined?

- The High Cost of Minimum Payments: Illustrative examples showing the long-term financial implications.

- Strategies for Faster Debt Repayment: Practical approaches to reduce your balance quickly.

- Building Good Credit Habits: Preventing future debt accumulation.

- Exploring Debt Consolidation and Balance Transfers: Options for managing multiple debts.

- Seeking Professional Financial Advice: When to consult with a financial advisor.

Smooth Transition to the Core Discussion

Now that we understand the importance of managing credit card debt effectively, let’s dive into the specific details of minimum payments on a $600 balance and how to tackle it strategically.

Exploring the Key Aspects of Minimum Payments on a $600 Credit Card

1. Definition and Core Concepts:

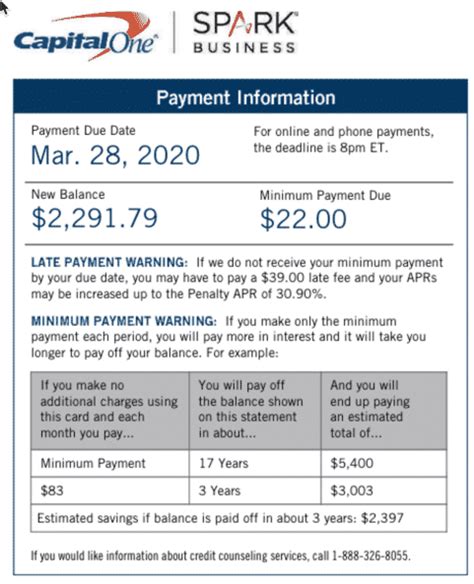

The minimum payment on a credit card is the smallest amount a cardholder is required to pay each billing cycle to avoid late payment fees and negative impacts on their credit report. This amount is typically a percentage of the outstanding balance (often 1-3%), but never less than a fixed minimum dollar amount (often around $25-$35). For a $600 balance, the minimum payment might fall anywhere within this range, depending on the specific terms of your credit card agreement. It’s crucial to check your statement each month to determine the exact amount.

2. Applications Across Industries:

The concept of minimum payments isn’t limited to a single industry. Credit card companies across the board employ this strategy, and the principles apply regardless of the brand. However, interest rates and minimum payment calculations may vary slightly between issuers.

3. Challenges and Solutions:

The primary challenge with minimum payments is the accumulation of interest. Paying only the minimum means a larger portion of your payment goes towards interest, leaving a smaller amount to reduce the principal balance. This leads to slow repayment and significantly higher total costs over the lifetime of the debt. Solutions include paying more than the minimum each month, exploring debt consolidation options, or working with a credit counselor to develop a repayment plan.

4. Impact on Innovation (Credit Scoring and Financial Products):

The widespread use of minimum payments has led to innovations in credit scoring models and financial products designed to help consumers manage debt. Credit scores now take into account payment history, demonstrating the importance of timely payments. Financial institutions have developed tools and resources such as debt management programs and balance transfer options to assist consumers in reducing their debt burden.

Closing Insights: Summarizing the Core Discussion

Understanding minimum payments is crucial for responsible credit card management. While convenient in the short term, consistently paying only the minimum on a $600 balance, or any balance, can lead to prolonged debt and significantly higher overall costs. Proactive strategies like paying more than the minimum, exploring debt consolidation, or seeking professional financial advice are essential for escaping the debt trap and building healthy financial habits.

Exploring the Connection Between Interest Rates and Minimum Payments on a $600 Credit Card

The interest rate on your credit card directly impacts how quickly your balance grows and how much you’ll ultimately pay. A higher interest rate will mean a larger portion of your minimum payment goes towards interest, making it harder to reduce the principal balance. Let’s explore this critical connection:

Key Factors to Consider:

-

Roles and Real-World Examples: A $600 balance with a 20% APR will accrue significantly more interest than the same balance with a 10% APR. This means your minimum payment will cover a larger portion of interest, leaving less to reduce the principal, extending your repayment period.

-

Risks and Mitigations: The risk of prolonged debt and significantly increased total costs is high with higher interest rates. Mitigation strategies include aggressively paying down the balance, exploring balance transfers to a lower-interest card, or negotiating a lower interest rate with your current issuer.

-

Impact and Implications: The long-term impact of high interest rates on your overall financial health is substantial. It can limit your ability to save, invest, and achieve other financial goals.

Conclusion: Reinforcing the Connection

The relationship between interest rates and minimum payments is crucial. Understanding how interest rates affect your minimum payment calculations is essential for making informed financial decisions and avoiding the debt trap. Taking proactive steps to manage your interest rate, such as securing a lower rate or paying down the balance quickly, can significantly improve your long-term financial health.

Further Analysis: Examining APR in Greater Detail

Annual Percentage Rate (APR) is the annual cost of borrowing, expressed as a percentage. Understanding your APR is critical because it dictates how much interest you'll pay on your outstanding balance. A higher APR means you’ll pay more interest over time, even if your minimum payment remains the same. This further emphasizes the importance of paying more than the minimum payment whenever possible.

FAQ Section: Answering Common Questions About Minimum Payments on a $600 Credit Card

-

What is the minimum payment on a $600 credit card? There’s no single answer; it depends on your credit card agreement, typically a percentage of the balance or a fixed minimum, whichever is greater. Always check your statement for the precise amount.

-

How is the minimum payment calculated? Most credit card companies calculate the minimum payment as a percentage of your outstanding balance (e.g., 2% or 3%), with a minimum dollar amount (e.g., $25).

-

What happens if I only pay the minimum payment? You'll accrue interest charges on your outstanding balance, extending your repayment period and increasing the total cost of your debt.

-

How can I pay off my credit card debt faster? Pay more than the minimum each month, explore balance transfers to lower-interest cards, or consider debt consolidation.

-

What if I can’t afford to make even the minimum payment? Contact your credit card issuer immediately to discuss your options, such as hardship programs or payment plans.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Management

-

Understand the Basics: Know your credit card agreement, including APR, minimum payment requirements, and late payment fees.

-

Budget Effectively: Create a realistic budget to allocate funds towards credit card repayment.

-

Pay More Than the Minimum: Even small extra payments significantly reduce the total interest paid and shorten the repayment period.

-

Track Your Spending: Monitor your expenses to avoid overspending and accumulating more debt.

-

Seek Professional Help: If struggling to manage debt, consult a credit counselor or financial advisor.

Final Conclusion: Wrapping Up with Lasting Insights

Minimum payments on a $600 credit card, while seemingly insignificant, can lead to a debt trap if consistently paid. Understanding how minimum payments are calculated, the impact of interest rates, and employing proactive repayment strategies are crucial for responsible credit card management. By proactively addressing debt, you protect your financial future and build a strong foundation for long-term financial well-being. Remember, responsible credit card usage is a cornerstone of healthy personal finance.

Latest Posts

Latest Posts

-

Money In Christianity

Apr 06, 2025

-

Does The Bible Talk About Money

Apr 06, 2025

-

Why Does The Bible Talk About Money So Much

Apr 06, 2025

-

How Much Does The Bible Talk About Money

Apr 06, 2025

-

What Does The Bible Said About Money

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Minimum Payment On 600 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.