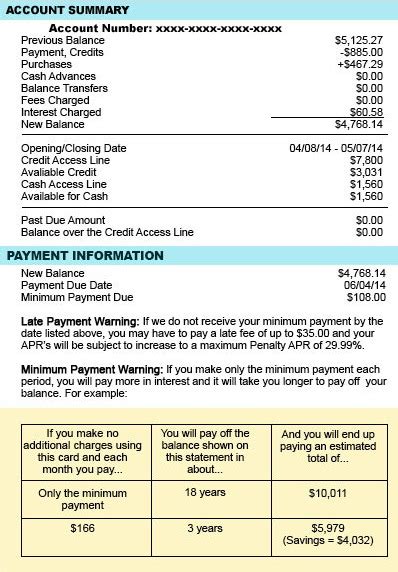

Minimum Monthly Payment Example

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Monthly Payment: Examples, Implications, and Strategies

What if the seemingly insignificant minimum monthly payment on your debt holds the key to financial freedom or crippling debt? Understanding its intricacies is crucial for navigating the complexities of personal finance.

Editor’s Note: This article on minimum monthly payments provides practical examples and actionable strategies to help you manage your debt effectively. Updated for 2024, this guide offers current insights into interest calculations and debt repayment strategies.

Why Minimum Monthly Payments Matter: Relevance, Practical Applications, and Industry Significance

Minimum monthly payments are the cornerstone of most credit agreements, from credit cards to mortgages and personal loans. While seemingly inconsequential, consistently only paying the minimum can lead to significantly higher overall costs due to accumulating interest. Conversely, understanding and strategically managing minimum payments can be the difference between financial stability and overwhelming debt. This understanding is crucial for consumers, impacting everything from credit scores to long-term financial goals. The implications extend across various industries, influencing lending practices, consumer behavior, and financial literacy initiatives.

Overview: What This Article Covers

This article dives deep into the world of minimum monthly payments, exploring how they're calculated, the long-term implications of only making minimum payments, and strategies for optimizing repayment plans. We'll examine various scenarios with illustrative examples, discuss the impact on credit scores, and offer practical tips for managing debt effectively. We will also explore the relationship between minimum payments and interest capitalization, highlighting the potential for snowballing debt.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing upon financial regulations, industry best practices, and real-world examples. Data on average interest rates, debt repayment timelines, and the impact of interest capitalization are sourced from reputable financial institutions and government agencies. The analysis aims to provide clear, accurate, and actionable insights for readers.

Key Takeaways:

- Understanding Minimum Payment Calculation: The formula and factors influencing minimum payments.

- Long-Term Cost of Minimum Payments: The significant financial implications of only making minimum payments.

- Strategies for Accelerated Debt Repayment: Methods to pay off debt faster and save money.

- Impact on Credit Scores: How payment behavior affects creditworthiness.

- Avoiding Interest Capitalization: Strategies to prevent interest from compounding and increasing your debt.

Smooth Transition to the Core Discussion:

Now that we understand the importance of minimum monthly payments, let's delve into the specifics, examining practical examples and strategies for effective debt management.

Exploring the Key Aspects of Minimum Monthly Payments

1. Definition and Core Concepts:

The minimum monthly payment is the smallest amount a borrower is required to pay on a debt each month to remain in good standing with the lender. This amount typically covers a portion of the principal balance (the original amount borrowed) and the accrued interest. The exact calculation varies depending on the type of debt (credit card, loan, mortgage) and the lender's policies.

2. Applications Across Industries:

Minimum monthly payment calculations are ubiquitous in the financial industry. They are used for:

- Credit Cards: Typically a percentage of the outstanding balance (often 2-3%), or a fixed minimum amount, whichever is greater.

- Personal Loans: Usually a fixed monthly payment calculated based on the loan amount, interest rate, and loan term.

- Mortgages: Similar to personal loans, with fixed monthly payments calculated using an amortization schedule.

- Student Loans: May have variable minimum payments depending on the loan type and repayment plan chosen.

3. Challenges and Solutions:

The primary challenge associated with minimum payments is the slow pace of debt repayment. Only making minimum payments significantly extends the repayment period, leading to substantially higher interest charges over time.

- Solution: Develop a budget to allocate more than the minimum payment towards debt repayment. Consider debt consolidation or balance transfer options to potentially lower interest rates.

4. Impact on Innovation:

The evolution of financial technology (FinTech) has led to innovative tools and apps designed to help consumers manage their debt more effectively, including budgeting apps, debt repayment calculators, and automated savings tools. These innovations contribute to increased financial literacy and empower consumers to make informed decisions about their debt.

Exploring the Connection Between Interest Rates and Minimum Monthly Payments

The relationship between interest rates and minimum monthly payments is critical. Higher interest rates translate to a larger portion of the minimum payment going towards interest, leaving less to reduce the principal.

Key Factors to Consider:

- Roles and Real-World Examples: A credit card with a $1,000 balance and a 20% interest rate will have a significantly higher minimum payment and a much slower repayment timeline compared to a card with the same balance but a 5% interest rate.

- Risks and Mitigations: High interest rates dramatically increase the total cost of borrowing and can lead to debt traps if only minimum payments are made. Mitigation strategies include refinancing to lower interest rates or aggressively paying down high-interest debt.

- Impact and Implications: Ignoring high interest rates leads to significantly increased long-term costs and can negatively impact credit scores due to prolonged debt.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum monthly payments underscores the importance of understanding interest calculations and employing effective debt management strategies. By proactively addressing high interest rates and employing various repayment methods, individuals can avoid the pitfalls of prolonged debt and achieve financial goals faster.

Further Analysis: Examining Interest Capitalization in Greater Detail

Interest capitalization occurs when accrued interest is added to the principal balance, increasing the overall amount owed. This can dramatically accelerate debt growth, especially if only minimum payments are made. For example, a credit card that charges interest on unpaid balances and then capitalizes that interest at the end of each billing cycle will rapidly increase the total debt. The longer the debt remains unpaid, the more significant the impact of capitalization becomes. Understanding this dynamic is crucial for avoiding a cycle of increasing debt.

FAQ Section: Answering Common Questions About Minimum Monthly Payments

- What is a minimum monthly payment? It's the smallest payment required to avoid default on a loan or credit account.

- How are minimum monthly payments calculated? The calculation varies by debt type and lender but generally includes a portion of the principal and accrued interest.

- What happens if I only pay the minimum monthly payment? You'll pay significantly more interest over time, extending the repayment period and increasing the total cost of borrowing.

- Can I pay more than the minimum monthly payment? Absolutely! Paying extra reduces your principal balance faster, saving you money on interest in the long run.

- What are the consequences of missing minimum payments? Late fees, higher interest rates, damage to your credit score, and potential account closure.

- How do minimum payments affect my credit score? Consistent on-time payments are crucial for a good credit score. Missing payments negatively impacts your score.

Practical Tips: Maximizing the Benefits of Understanding Minimum Monthly Payments

- Track Your Debt: Maintain a clear record of all your debts, including balances, interest rates, and minimum payments.

- Create a Budget: Allocate a portion of your income towards debt repayment, aiming for more than the minimum payment.

- Prioritize High-Interest Debt: Focus on paying down debts with the highest interest rates first to minimize long-term costs.

- Explore Debt Consolidation: Consider consolidating multiple debts into a single loan with a lower interest rate.

- Negotiate with Creditors: If you're struggling to make payments, contact your creditors to explore options like hardship programs or payment plans.

- Use Debt Repayment Calculators: These online tools can help you estimate how long it will take to pay off your debt and how much you'll save by paying extra.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding minimum monthly payments is a cornerstone of responsible financial management. While seemingly simple, the implications of consistently paying only the minimum can be financially devastating. By actively managing debt, prioritizing high-interest debts, and exploring various repayment strategies, individuals can break free from the cycle of accumulating debt and build a secure financial future. Take control of your finances today. The journey to financial freedom starts with understanding the seemingly small, yet impactful, minimum monthly payment.

Latest Posts

Latest Posts

-

What Is The Minimum Weekly Pip Payment

Apr 06, 2025

-

Whats The Minimum Amount Of Pip

Apr 06, 2025

-

What Is The Standard Payment For Pip

Apr 06, 2025

-

What Is The Lowest Payment For Pip

Apr 06, 2025

-

How Much Is Minimum Pip Payment

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Minimum Monthly Payment Example . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.