How To Figure Minimum Payment On Credit Card

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Decoding the Mystery: How to Figure Your Minimum Credit Card Payment

What if understanding your credit card minimum payment could save you thousands of dollars over your lifetime? Mastering this seemingly simple calculation is crucial for responsible credit card management and avoiding the debt trap.

Editor’s Note: This article on calculating minimum credit card payments was published today to provide readers with the most up-to-date information and strategies for managing their credit card debt effectively. Understanding your minimum payment is the first step towards financial health.

Why Understanding Your Minimum Credit Card Payment Matters:

Ignoring your minimum payment or misunderstanding its calculation can lead to a snowball effect of accumulating interest and fees, significantly impacting your credit score and financial well-being. Understanding this seemingly small detail empowers you to make informed decisions about your spending and repayment strategies, ultimately leading to better financial control. This knowledge is particularly important given the rising interest rates and the increasing prevalence of credit card debt. The information provided here can help you avoid costly mistakes and develop a solid foundation for responsible credit card management.

Overview: What This Article Covers:

This article will demystify the minimum credit card payment calculation. We'll explore how credit card companies determine this amount, common misconceptions surrounding it, and strategies for managing your payments effectively. We will also examine the impact of late payments and explore alternative repayment options. Finally, we'll address frequently asked questions and offer practical tips for maximizing your financial well-being.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing upon information from leading financial institutions, consumer protection agencies, and personal finance experts. We've analyzed various credit card agreements, examined industry best practices, and consulted reputable sources to ensure accuracy and provide readers with reliable and actionable insights.

Key Takeaways:

- Understanding the Calculation: We’ll break down the different methods credit card companies use to determine minimum payments.

- Common Misconceptions: We’ll debunk common myths surrounding minimum payments and their impact.

- Managing Payments Effectively: We'll discuss strategies for making timely payments and minimizing interest charges.

- Avoiding Late Fees: We’ll explain the consequences of late payments and how to prevent them.

- Alternative Repayment Options: We'll explore options like balance transfers and debt consolidation.

Smooth Transition to the Core Discussion:

Now that we understand the importance of grasping minimum payment calculations, let's delve into the specifics and equip you with the knowledge to navigate your credit card statements with confidence.

Exploring the Key Aspects of Minimum Credit Card Payments:

1. How Credit Card Companies Calculate Minimum Payments:

There's no single universal formula. Methods vary across issuers, but generally involve a combination of factors:

-

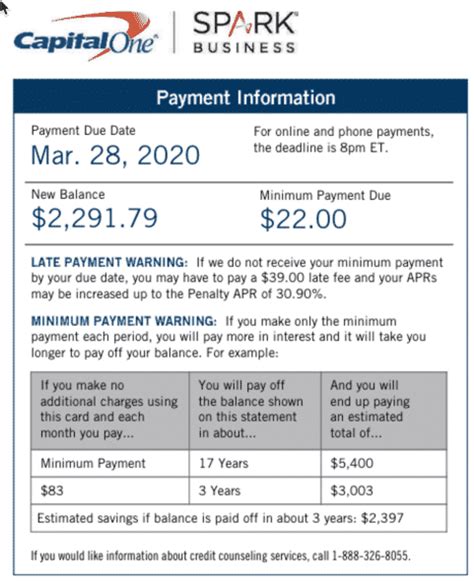

A Percentage of Your Balance: This is the most common method. Credit card companies typically set a minimum payment as a percentage of your outstanding balance (often 1% to 3%, but this can vary). For example, on a $1000 balance, a 2% minimum payment would be $20.

-

A Minimum Dollar Amount: Some issuers have a minimum dollar amount, regardless of the balance. This might be set at $25 or $35, ensuring a minimum payment even on smaller balances.

-

Interest Accrued: In addition to the percentage or minimum dollar amount, the minimum payment often includes the interest accrued during the billing cycle. This means the minimum payment doesn't just cover a portion of the principal balance; it also covers the interest charged. Failing to pay this interest will lead to a rapidly growing debt.

-

Fees: Any late fees, over-limit fees, or other charges incurred during the billing cycle will also be included in the minimum payment.

2. Common Misconceptions about Minimum Payments:

-

Myth 1: Paying the Minimum is Enough: This is a dangerous misconception. While paying the minimum prevents immediate delinquency, it keeps you locked in a cycle of high interest payments, extending the repayment period and significantly increasing the total cost. The vast majority of the payment goes towards interest, leaving little to reduce the principal balance.

-

Myth 2: Minimum Payments are Fixed: They are not. Minimum payments can fluctuate depending on your outstanding balance, interest charges, and fees. Always check your statement carefully.

-

Myth 3: Paying the Minimum Improves Credit Score: While avoiding late payments is crucial for a good credit score, simply paying the minimum won't boost it significantly. Paying more than the minimum and consistently reducing your debt is key to improving your credit health.

3. Managing Payments Effectively:

-

Always Pay on Time: Late payments severely damage your credit score and incur additional fees. Set up automatic payments to avoid missed deadlines.

-

Pay More Than the Minimum: The best way to reduce debt faster is to pay more than the minimum payment each month. Even an extra $20 or $50 can make a considerable difference over time.

-

Budgeting and Financial Planning: Create a realistic budget to track your spending and ensure you can afford your credit card payments. Consider using budgeting apps or spreadsheets to stay organized.

-

Track Your Spending: Monitor your credit card spending to avoid overspending and accumulating unnecessary debt.

4. The Impact of Late Payments:

Late payments trigger a cascade of negative consequences:

-

Late Fees: Expect substantial fees, often ranging from $25 to $40 or more.

-

Damaged Credit Score: Late payments significantly lower your credit score, making it harder to obtain loans, rent apartments, or even secure favorable insurance rates.

-

Increased Interest Rates: Some credit card companies may increase your interest rate due to consistent late payments, further escalating your debt.

-

Collection Agencies: Persistent late payments can lead to your account being sent to collections, severely harming your credit history.

Exploring the Connection Between Interest Rates and Minimum Payments:

The relationship between interest rates and minimum payments is profoundly significant. Higher interest rates mean a larger portion of your minimum payment goes towards interest, leaving less to reduce the principal balance. This can trap you in a cycle of debt where you struggle to reduce your balance despite making consistent payments. Understanding this connection is crucial for planning effective repayment strategies.

Key Factors to Consider:

-

Roles and Real-World Examples: A person with a high interest rate and a large balance might find their minimum payment mostly covers interest, barely making a dent in the principal. Conversely, someone with a low balance and low interest might find a larger portion of their minimum payment goes towards the principal.

-

Risks and Mitigations: High interest rates pose a significant risk of prolonged debt. Mitigation strategies include balance transfers to lower-interest cards, debt consolidation loans, or seeking professional financial advice.

-

Impact and Implications: High interest rates extend the repayment period, leading to significantly higher total interest payments. This impacts long-term financial goals, such as saving for a house or retirement.

Conclusion: Reinforcing the Connection:

The interplay between interest rates and minimum payments underscores the importance of understanding your credit card statement thoroughly. By proactively managing your spending, choosing cards with lower interest rates, and consistently paying more than the minimum, you can mitigate the risks associated with high interest and achieve better financial outcomes.

Further Analysis: Examining Interest Rates in Greater Detail:

Understanding how interest rates are calculated and the factors that influence them provides further insights into managing your credit card debt effectively. Different card issuers have different interest rate structures, which can impact the amount you pay over the life of your debt. Researching various cards and understanding your creditworthiness can help you secure a more favorable interest rate.

FAQ Section: Answering Common Questions About Minimum Credit Card Payments:

-

Q: What happens if I only pay the minimum payment for an extended period? A: You’ll pay significantly more in interest over time, extending the repayment period and increasing the total cost of your debt.

-

Q: Can I negotiate a lower minimum payment with my credit card company? A: It's unlikely, but you can try contacting customer service to discuss your financial situation and explore options like a hardship program.

-

Q: What if I miss a minimum payment? A: You'll likely incur late fees, damage your credit score, and potentially face higher interest rates.

-

Q: How can I find out my minimum payment amount? A: Your minimum payment is clearly stated on your monthly credit card statement.

Practical Tips: Maximizing the Benefits of Understanding Your Minimum Payment:

-

Read Your Statement Carefully: Understand the breakdown of your minimum payment, including principal, interest, and fees.

-

Budget Strategically: Allocate sufficient funds each month to pay more than the minimum.

-

Explore Debt Reduction Strategies: Consider balance transfers, debt consolidation, or seeking professional financial guidance.

-

Set Reminders: Use online banking tools or calendar reminders to ensure timely payments.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding how to figure your minimum credit card payment is foundational to responsible credit card management. While it may seem like a small detail, its impact on your overall financial health is significant. By actively managing your payments, paying more than the minimum, and understanding the interplay between interest rates and minimum payments, you can avoid the debt trap and build a solid financial future. Take control of your finances today by mastering this essential calculation.

Latest Posts

Latest Posts

-

How To Become A Money Manager

Apr 06, 2025

-

Activities For Money Management

Apr 06, 2025

-

Fun Money Management Activities For Adults

Apr 06, 2025

-

How To Make Personal Finance Fun

Apr 06, 2025

-

What Is Electronic Money

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about How To Figure Minimum Payment On Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.