How Many Grace Periods For Student Loans

adminse

Apr 01, 2025 · 8 min read

Table of Contents

How Many Grace Periods Are Available for Student Loans?

Navigating the Complexities of Student Loan Deferments and Forbearances

Editor’s Note: This article on student loan grace periods, deferments, and forbearances was published today, providing readers with up-to-date information on this critical aspect of student loan repayment. Understanding these options is crucial for borrowers to manage their debt effectively and avoid delinquency.

Why Understanding Grace Periods Matters:

Student loan repayment can be daunting. The sheer volume of debt, coupled with the transition into the workforce, can leave recent graduates feeling overwhelmed. Knowledge of grace periods, deferments, and forbearances is vital for responsible financial management. This knowledge empowers borrowers to make informed decisions, avoid negative impacts on their credit scores, and strategically manage their debt repayment journey. This article will clarify the nuances of these financial tools, helping borrowers navigate the complexities of student loan repayment.

Overview: What This Article Covers:

This article provides a comprehensive overview of student loan grace periods, differentiating them from deferments and forbearances. It examines the eligibility criteria, duration, and implications of each option. Furthermore, it delves into the specific grace periods offered for different types of federal student loans, and explores the potential consequences of missing payments during and after a grace period. Finally, the article offers practical advice for borrowers to effectively utilize these repayment options.

The Research and Effort Behind the Insights:

This article is based on extensive research, drawing information from official government websites, such as the Federal Student Aid website (studentaid.gov), and reputable financial publications. It incorporates information from government regulations and official documentation to ensure accuracy and provide readers with reliable, up-to-date insights.

Key Takeaways:

- Definition of Grace Periods: A grace period is a temporary period after graduation or leaving school where borrowers are not required to make loan payments.

- Types of Student Loans and Grace Periods: Different types of federal student loans offer varying grace periods.

- Deferments vs. Forbearances: Understanding the key differences between these options is crucial for choosing the most suitable path.

- Consequences of Missed Payments: The consequences of failing to make payments during and after the grace period are significant and can have long-term effects.

- Strategies for Effective Loan Management: Practical tips for borrowers to manage their loans effectively and avoid delinquency.

Smooth Transition to the Core Discussion:

With a clear understanding of the importance of understanding grace periods, let's delve deeper into the specifics of federal student loan repayment options. We will first explore the concept of grace periods and then differentiate them from deferments and forbearances.

Exploring the Key Aspects of Student Loan Grace Periods, Deferments, and Forbearances:

1. Grace Periods:

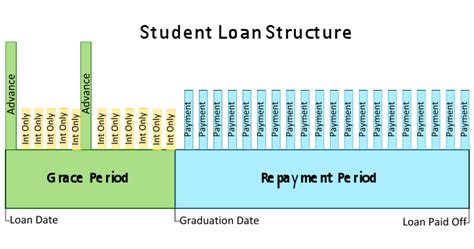

A grace period is a temporary reprieve from student loan repayment. It's a period of time after you leave school (graduate, withdraw, or drop below half-time enrollment) before you are required to begin making payments on your federal student loans. The length of the grace period varies depending on the type of loan.

2. Federal Student Loan Grace Periods:

- Direct Subsidized Loans and Unsubsidized Loans: These loans generally have a six-month grace period. During this time, interest does not accrue on subsidized loans, but it does accrue on unsubsidized loans.

- Direct PLUS Loans: These loans typically have no grace period. Repayment begins immediately upon disbursement or soon after, depending on the terms.

- FFEL Program Loans: These loans may have different grace periods depending on when they were taken out and their specific terms. Information on FFEL Program loans may require contacting the loan servicer directly.

3. Deferments:

Deferments are temporary postponements of your student loan payments. Unlike grace periods, which are automatic for most federal student loans, deferments must be applied for and are typically granted under specific circumstances. These circumstances might include unemployment, economic hardship, or enrollment in graduate school. Interest may or may not accrue during a deferment period, depending on the type of loan and the reason for deferment.

4. Forbearances:

Forbearances are similar to deferments, in that they temporarily suspend your loan payments. However, forbearance is generally granted when a borrower experiences temporary financial hardship that prevents them from making payments, even if they do not meet the criteria for a deferment. Interest usually accrues during a forbearance, and this accumulated interest is added to the principal loan balance, increasing the total amount owed.

5. Key Differences Between Grace Periods, Deferments, and Forbearances:

| Feature | Grace Period | Deferment | Forbearance |

|---|---|---|---|

| Automatic? | Usually (for federal loans) | No, requires application | No, requires application |

| Eligibility | Graduation/leaving school | Specific circumstances (e.g., unemployment, graduate school) | Financial hardship |

| Interest | Varies (often none on subsidized loans) | Varies (can be capitalized) | Usually accrues |

| Duration | Typically 6 months (federal) | Varies (up to 3 years in some cases) | Varies (typically shorter periods) |

Exploring the Connection Between Loan Type and Grace Period Length:

The type of student loan significantly impacts the length of the grace period. Direct Subsidized Loans offer a grace period where interest is not charged, encouraging timely repayment. This contrasts with Direct Unsubsidized Loans, where interest accrues during the grace period, potentially leading to a larger principal amount upon repayment commencement. Understanding this difference allows borrowers to plan their finances accordingly. Direct PLUS loans, often taken out by parents, usually don't offer a grace period.

Key Factors to Consider:

Roles and Real-World Examples:

A student graduating with a Direct Subsidized Loan has a six-month grace period. However, a student with a Direct PLUS loan has no such grace period and must start repayments immediately. Understanding this is crucial for budget planning. A graduate facing unexpected unemployment may apply for a deferment, temporarily halting payments and preventing delinquency.

Risks and Mitigations:

Failing to make payments after the grace period ends can result in delinquency, negatively impacting your credit score and potentially leading to wage garnishment or tax refund offset. To mitigate this risk, borrowers should create a realistic repayment plan, explore options like income-driven repayment plans, and contact their loan servicer if facing financial difficulties.

Impact and Implications:

The length of the grace period and the choice to utilize deferments or forbearances significantly influence the total cost of a student loan. Accumulated interest during forbearance periods can increase the overall debt, while strategic use of deferments can provide much-needed financial breathing room.

Conclusion: Reinforcing the Connection:

The connection between loan type and grace period, along with the availability of deferments and forbearances, underscores the importance of understanding your specific loan terms. Careful planning, proactive communication with your loan servicer, and awareness of the potential consequences of missed payments are crucial for responsible student loan management.

Further Analysis: Examining Income-Driven Repayment Plans:

Income-driven repayment (IDR) plans are designed to make student loan payments more manageable based on your income and family size. These plans offer lower monthly payments than standard repayment plans, and often extend the repayment period. While this might result in paying more interest over the loan's life, it can be a lifesaver for borrowers facing financial hardship. Exploring IDR plans may prevent default and alleviate the stress of overwhelming monthly payments.

FAQ Section: Answering Common Questions About Student Loan Grace Periods:

What happens if I don't make payments after my grace period ends?

Failing to make payments after your grace period will result in delinquency, negatively impacting your credit score. Further delinquency can lead to collection actions, including wage garnishment or tax refund offset.

Can I extend my grace period?

Grace periods are generally not extendable. However, you might be eligible for a deferment or forbearance if facing financial hardship.

What is the difference between a deferment and a forbearance?

Deferments are typically granted for specific reasons (e.g., unemployment, graduate school), and interest may or may not accrue. Forbearances are granted for financial hardship, and interest usually accrues.

How do I apply for a deferment or forbearance?

You must contact your loan servicer to apply for a deferment or forbearance. They will guide you through the application process and provide the necessary documentation.

Practical Tips: Maximizing the Benefits of Grace Periods and Other Repayment Options:

- Understand Your Loan Terms: Familiarize yourself with the type of loan you have, the length of your grace period, and the interest rates.

- Budget Carefully: Create a realistic budget that includes your student loan payments (once the grace period ends).

- Explore Repayment Options: Consider income-driven repayment plans or other repayment options if your standard payments are too high.

- Communicate with Your Servicer: Contact your loan servicer promptly if you anticipate difficulty making payments. They can offer solutions to prevent delinquency.

Final Conclusion: Wrapping Up with Lasting Insights:

Navigating the complexities of student loan repayment requires a thorough understanding of grace periods, deferments, and forbearances. By understanding the differences between these options and taking proactive steps to manage your debt, you can avoid delinquency, protect your credit score, and ultimately achieve financial success. Remember to utilize resources provided by the Federal Student Aid website and communicate openly with your loan servicer. Effective financial planning is key to successful student loan repayment.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On A 5000 Credit Card Balance

Apr 04, 2025

-

What Is The Minimum Payment On A 5000 Credit Card Uk

Apr 04, 2025

-

How To Pass Optus Credit Check

Apr 04, 2025

-

How To Pass Telstra Credit Check

Apr 04, 2025

-

How To Pass Credit Check For Phone

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about How Many Grace Periods For Student Loans . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.