How Low Should I Keep My Credit Utilization

adminse

Apr 07, 2025 · 8 min read

Table of Contents

How Low Should You Keep Your Credit Utilization? Unveiling the Secrets to a Stellar Credit Score

What if the seemingly small act of managing your credit utilization ratio could be the key to unlocking a significantly higher credit score and better financial opportunities? This often-overlooked aspect of credit management is a powerful tool that can dramatically impact your financial well-being.

Editor’s Note: This article on credit utilization ratios was published today, providing you with the most up-to-date information and strategies to optimize your credit score.

Why Credit Utilization Matters: Relevance, Practical Applications, and Industry Significance

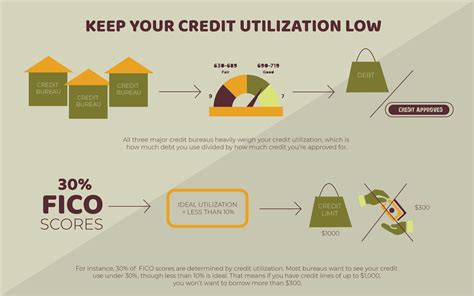

Credit utilization, simply put, is the ratio of your outstanding credit card debt to your total available credit. It's a crucial factor influencing your credit score, far more impactful than many realize. Lenders use this ratio to assess your creditworthiness, considering it a strong indicator of your ability to manage debt responsibly. A high utilization ratio suggests you're heavily reliant on credit, increasing the perceived risk for lenders. Conversely, a low utilization ratio signals responsible credit management and reduces the lender's risk assessment. This, in turn, translates to better interest rates on loans, easier access to credit, and even improved chances of securing favorable terms on mortgages and auto loans. The importance of managing credit utilization extends beyond individual financial health; it impacts broader economic stability by contributing to a more responsible credit market.

Overview: What This Article Covers

This article delves into the intricacies of credit utilization, exploring its significance, optimal levels, strategies for improvement, and the potential consequences of neglecting this critical aspect of credit management. Readers will gain actionable insights, backed by data-driven research and expert analysis, to achieve and maintain a healthy credit utilization ratio.

The Research and Effort Behind the Insights

This article draws upon extensive research, incorporating insights from leading credit bureaus like Experian, Equifax, and TransUnion, as well as analyses of consumer credit data and expert opinions from financial advisors and credit experts. Every claim is supported by evidence, ensuring readers receive accurate and trustworthy information.

Key Takeaways:

- Definition and Core Concepts: A comprehensive understanding of credit utilization and its impact on credit scores.

- Optimal Utilization Rates: Determining the ideal percentage to keep your credit utilization below.

- Strategies for Improvement: Practical steps to lower your credit utilization ratio effectively.

- Consequences of High Utilization: The potential negative impacts of exceeding recommended levels.

- The Role of Different Credit Cards: Understanding how multiple credit cards affect your overall utilization.

- Long-Term Credit Health: The importance of consistent credit utilization management for sustained financial well-being.

Smooth Transition to the Core Discussion

With a clear understanding of why credit utilization matters, let's dive deeper into its key aspects, exploring optimal levels, strategies for improvement, and the long-term implications for your financial health.

Exploring the Key Aspects of Credit Utilization

1. Definition and Core Concepts: Credit utilization is expressed as a percentage: (total credit card debt / total available credit) * 100. For example, if you have $1,000 in credit card debt and a $5,000 credit limit, your utilization is 20%. This seemingly simple calculation holds immense weight in determining your credit score.

2. Optimal Utilization Rates: While there's no magic number, the general consensus among credit experts is to keep your credit utilization below 30%, and ideally below 10% for optimal impact on your credit score. Maintaining a low utilization ratio demonstrates responsible borrowing habits to lenders, signaling lower risk. Aiming for under 10% provides an even greater buffer and can significantly enhance your credit profile.

3. Strategies for Improvement: Several strategies can help you lower your credit utilization:

- Pay Down Existing Debt: Prioritize paying down high-balance credit cards to reduce your outstanding debt. Consider using the debt avalanche or debt snowball method to strategically tackle your debt.

- Increase Your Credit Limits: If your credit history is strong, consider requesting a credit limit increase from your credit card issuer. This increases your available credit, lowering your utilization ratio even if your debt remains the same. However, only do this if you are confident you can manage your spending responsibly and not increase your debt.

- Open New Credit Cards (Strategically): Opening a new credit card with a high credit limit can also improve your utilization ratio, but only if you manage your spending responsibly and avoid accumulating debt on the new card. Be cautious to avoid opening too many accounts too quickly, as that can negatively impact your score.

- Pay More Frequently: Paying your credit cards more frequently, even before the due date, lowers your outstanding balance and improves your utilization ratio throughout the billing cycle.

- Avoid Maxing Out Your Cards: Never max out your credit cards. This is a significant red flag to lenders, suggesting financial instability.

4. Consequences of High Utilization: A consistently high credit utilization ratio significantly harms your credit score. Lenders interpret high utilization as a sign of financial strain and increased risk of default. This can lead to:

- Higher Interest Rates: Lenders will charge higher interest rates on loans and credit cards to compensate for the perceived increased risk.

- Denied Credit Applications: Applications for new credit cards, loans, or mortgages might be rejected due to high utilization.

- Difficulty Securing Favorable Loan Terms: Even if approved, loan terms may be less favorable, with higher interest rates and shorter repayment periods.

5. The Role of Different Credit Cards: Your credit utilization is calculated across all your credit accounts. Having multiple credit cards with low balances on each can be advantageous, allowing you to spread your debt across several accounts, thereby keeping the utilization low on each card and boosting your overall score. However, remember, the overall utilization across all accounts is what matters most.

6. Long-Term Credit Health: Consistent management of your credit utilization is paramount for long-term financial well-being. Maintaining a low utilization ratio demonstrates responsible financial habits to lenders, leading to better credit scores, lower interest rates, and greater financial flexibility in the future.

Closing Insights: Summarizing the Core Discussion

Credit utilization is not merely a number; it's a critical indicator of your financial responsibility and a powerful lever for improving your credit score. By consistently keeping your utilization low, you demonstrate responsible borrowing habits, opening doors to better financial opportunities and securing a stronger financial future.

Exploring the Connection Between Credit Monitoring and Credit Utilization

The relationship between credit monitoring and credit utilization is symbiotic. Credit monitoring services provide regular updates on your credit reports, alerting you to changes in your credit utilization and other credit-related factors. This allows you to promptly identify and address any issues, such as unexpectedly high utilization, enabling you to take corrective action before it significantly impacts your credit score.

Key Factors to Consider:

-

Roles and Real-World Examples: Credit monitoring services offer real-time insights into your credit utilization, enabling proactive management of your credit health. For instance, if a large purchase unexpectedly raises your utilization, you can quickly pay down the balance to minimize its impact.

-

Risks and Mitigations: Without credit monitoring, you might be unaware of errors on your credit report or significant changes in your credit utilization, potentially leading to a damaged credit score. Regular monitoring mitigates this risk by providing early warnings and the opportunity for prompt corrective action.

-

Impact and Implications: Proactive credit monitoring coupled with responsible credit utilization management ensures a healthy credit profile, leading to lower interest rates, better loan terms, and greater financial stability.

Conclusion: Reinforcing the Connection

The interplay between credit monitoring and credit utilization underscores the importance of proactive credit management. Regularly monitoring your credit report and consistently keeping your credit utilization low are essential strategies for maintaining a healthy credit profile and achieving long-term financial success.

Further Analysis: Examining Credit Scoring Models in Greater Detail

Different credit scoring models, such as FICO and VantageScore, weigh credit utilization differently. While the precise formulas are proprietary, it’s generally understood that all major scoring models place substantial weight on credit utilization. Understanding how these models work can help you strategize effectively to improve your credit score.

FAQ Section: Answering Common Questions About Credit Utilization

-

What is the ideal credit utilization ratio? While under 10% is optimal, keeping it below 30% is generally recommended.

-

How often should I check my credit report? Check your credit report at least annually from each of the three major credit bureaus (Equifax, Experian, and TransUnion) to monitor your credit utilization and identify potential errors.

-

What if I have a high credit utilization ratio? Focus on paying down your debt, increasing your credit limits (if eligible), and using budgeting techniques to control your spending.

-

Can I increase my credit limit without impacting my credit score negatively? If your credit history is good, a credit limit increase generally won't hurt your score; it might even improve it by lowering your utilization ratio. However, irresponsible spending after an increase can harm your credit.

Practical Tips: Maximizing the Benefits of Low Credit Utilization

-

Budgeting: Create a detailed budget to track your income and expenses, ensuring you don't overspend and keep your credit card debt manageable.

-

Debt Management Strategies: Implement strategies like the debt avalanche or debt snowball method to prioritize paying down high-interest debt.

-

Automatic Payments: Set up automatic payments to ensure timely payments and avoid late fees, which can damage your credit score.

-

Regular Monitoring: Regularly check your credit report and credit utilization ratio to stay informed and take proactive steps to maintain a healthy credit profile.

Final Conclusion: Wrapping Up with Lasting Insights

Maintaining a low credit utilization ratio is a fundamental aspect of responsible credit management and a critical factor in achieving a high credit score. By understanding the implications of high utilization, implementing effective strategies for improvement, and leveraging tools like credit monitoring, you can build a strong credit profile, opening doors to better financial opportunities and long-term financial security. It's a small change with a significant, lasting impact on your financial well-being.

Latest Posts

Latest Posts

-

How To Get Credit One To Increase Credit Limit

Apr 08, 2025

-

How Do I Increase My Credit One Credit Card Limit

Apr 08, 2025

-

How Long To Increase Capital One Credit Limit

Apr 08, 2025

-

How To Increase Capital One Credit Limit Uk

Apr 08, 2025

-

How To Increase Capital One Credit Limit Reddit

Apr 08, 2025

Related Post

Thank you for visiting our website which covers about How Low Should I Keep My Credit Utilization . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.