How Long Does Paid Off Collections Stay On Credit Report

adminse

Apr 07, 2025 · 7 min read

Table of Contents

How Long Do Paid-Off Collections Stay on Your Credit Report? Unlocking the Secrets to Credit Repair

How long will a blemish on my credit report, even after I've paid it, continue to haunt my financial future?

Understanding the lifespan of paid collections on your credit report is crucial for building strong credit and achieving your financial goals.

Editor's Note: This article provides up-to-date information on how long paid collections remain on credit reports. The information presented here is for educational purposes and should not be considered legal or financial advice. Always consult with a qualified professional for personalized guidance.

Why Paid Collections Matter: The Lingering Shadow on Your Credit Score

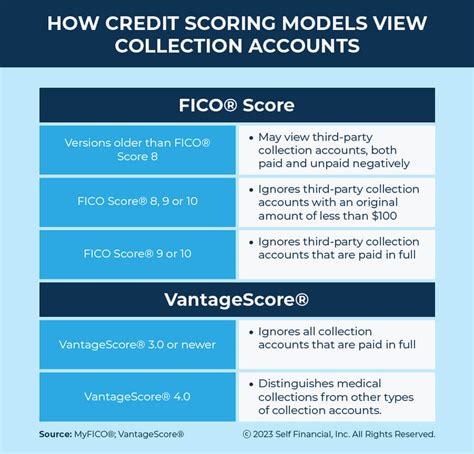

A collection account appears on your credit report when a creditor sells a delinquent debt to a collections agency. Even after diligently paying off this debt, the record remains, casting a long shadow on your creditworthiness. This lingering negative mark can significantly impact your ability to secure loans, rent an apartment, or even get a job. Understanding the timeline of its presence is paramount to effective credit repair. The impact extends beyond your credit score; it can also affect your insurance premiums and even your chances of getting approved for certain services.

Overview: What This Article Covers

This comprehensive guide delves into the intricacies of paid collection accounts on your credit report. We'll explore the typical lifespan of these entries, the factors influencing their duration, strategies for expediting their removal, and the importance of proactive credit monitoring. This article also addresses common misconceptions and provides practical advice for navigating this complex aspect of credit management.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing upon the Fair Credit Reporting Act (FCRA), analysis of credit reporting agency practices, and insights from financial experts. Data from reputable sources, including consumer finance websites and legal documents, have been meticulously analyzed to ensure accuracy and provide readers with a well-informed perspective.

Key Takeaways:

- Standard Duration: Generally, paid collections remain on your credit report for seven years from the date of the original delinquency, not the date of payment.

- Exceptions Exist: Certain circumstances, such as bankruptcy or identity theft, might alter this timeframe.

- Accuracy is Key: Disputing inaccurate information on your credit report is crucial for potential removal.

- Proactive Monitoring: Regular credit report checks are essential for identifying and addressing any errors.

- Future Implications: Understanding the impact of paid collections can help you make informed financial decisions.

Smooth Transition to the Core Discussion:

Now that we understand the importance of this topic, let's delve deeper into the specifics of how long paid collections stay on your credit report and what steps can be taken to mitigate their negative impact.

Exploring the Key Aspects of Paid Collection Account Lifespans

1. The Seven-Year Rule: The FCRA generally dictates that negative information, including paid collections, remains on your credit report for seven years from the date of the original delinquency. This is the date the account first went into default, not the date you paid it off. This means even after making a payment in full, the negative mark will remain visible for a considerable period.

2. Exceptions to the Rule:

- Bankruptcy: Bankruptcy filings have their own reporting timelines, typically 7-10 years, impacting the reporting period for related debts.

- Identity Theft: If the collection stems from identity theft, the account's duration on your report may be shorter if successfully disputed and resolved.

- Inaccurate Information: If you can demonstrate that the information reported is factually incorrect, you can initiate a dispute with the credit bureau to have it removed.

3. The Role of Credit Reporting Agencies: Three major credit bureaus—Equifax, Experian, and TransUnion—compile and maintain your credit report. While they follow the FCRA guidelines, their individual processes and timelines may slightly vary, but generally align with the seven-year rule.

4. The Impact on Your Credit Score: Paid collections, even after being paid, negatively influence your credit score. The longer they remain on your report, the more significant their impact, delaying your access to favorable credit terms.

5. Dispute Process: The FCRA provides consumers with the right to dispute inaccurate or incomplete information on their credit reports. If a paid collection account is reported incorrectly or includes outdated information, you can leverage this right to pursue its removal.

Exploring the Connection Between Timely Payment and Collection Account Lifespan

While prompt payment is crucial for avoiding collections altogether, it doesn't alter the seven-year reporting period for already-existing paid collections. Timely payments on current accounts positively impact your credit score and demonstrate financial responsibility, counteracting the negative effects of past collections. However, it's important to differentiate between preventing future collections and influencing the removal of existing ones.

Key Factors to Consider:

- Roles and Real-World Examples: Consider a situation where an individual pays off a medical collection after three years of delinquency. The collection will still remain on their credit report for four more years from the original delinquency date, despite the prompt payment.

- Risks and Mitigations: Failing to dispute inaccurate information increases the risk of the collection remaining on your report longer than necessary. Mitigation involves meticulously reviewing your credit report and promptly filing disputes when needed.

- Impact and Implications: The longer a paid collection remains, the more difficult it becomes to secure favorable loan terms or obtain lower interest rates.

Conclusion: Reinforcing the Connection Between Payment and Reporting Period

The relationship between timely payment and a paid collection's lifespan is indirect. While responsible financial management prevents future collections, it doesn't directly reduce the reporting time for past ones. Focusing on accurate reporting and disputing errors is critical to removing inaccurate or outdated information as quickly as possible.

Further Analysis: Examining the Dispute Process in Greater Detail

Dispute processes vary slightly across credit bureaus. Generally, the process involves submitting a written dispute detailing the inaccuracies or incompleteness of the collection account information. Providing supporting documentation, such as payment receipts or proof of identity theft, strengthens your case. The credit bureau will investigate and, if the information is deemed inaccurate, will correct or remove the entry.

FAQ Section: Answering Common Questions About Paid Collections

Q: What if I can't afford to pay off the collection immediately?

A: Negotiate a payment plan with the collection agency. While this doesn't change the reporting period, it demonstrates responsibility and may improve your credit standing over time.

Q: How often should I check my credit report?

A: At least annually, or even quarterly if you have experienced financial difficulties or suspect identity theft.

Q: What if the collection agency won't remove the paid collection after seven years?

A: Contact the credit bureau directly and reiterate your dispute. If that doesn't work, consider consulting a credit repair specialist or attorney.

Practical Tips: Maximizing the Benefits of Credit Report Accuracy

-

Monitor Regularly: Access your free credit reports annually from AnnualCreditReport.com to monitor for errors.

-

Dispute Promptly: Don't hesitate to dispute inaccurate information; the sooner you act, the better.

-

Maintain Good Credit Habits: Consistently make timely payments on all accounts to offset the negative impact of past collections.

-

Consider Credit Counseling: If you are struggling with debt, consider seeking professional credit counseling.

-

Build Positive Credit History: Over time, new positive credit accounts will outweigh the negative impact of paid collections.

Final Conclusion: Navigating the Path to Credit Restoration

Paid collections cast a long shadow, but understanding their lifespan and actively managing your credit report can significantly mitigate their effects. By staying informed, proactive, and vigilant, individuals can navigate the complexities of credit repair and rebuild their financial well-being. Remember, while the seven-year rule applies, proactive steps such as meticulous credit monitoring and prompt dispute resolution can significantly shorten the period of negative impact. Financial success is achievable even after facing past financial challenges.

Latest Posts

Latest Posts

-

How Much Does A Car Loan Build Credit

Apr 08, 2025

-

How Fast Does Car Payment Build Credit

Apr 08, 2025

-

How Fast Does A Car Payment Build Your Credit

Apr 08, 2025

-

When Does Lowes Credit Card Report To Credit Bureaus

Apr 08, 2025

-

When Does Kohls Credit Card Report To Credit Bureaus

Apr 08, 2025

Related Post

Thank you for visiting our website which covers about How Long Does Paid Off Collections Stay On Credit Report . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.